42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Nomura: The Tightening Of Global Financial Conditions Will Not Stop Until…

Despite all the hand-wringing and teeth-gnashing about lower asset prices – and “won’t someone do something?” – Nomura’s Charlie McElligott warns that the recent impulse tightening in global Financial Conditions (largely via US Dollar and Real Rates) likely will not stop until one or more of the following three events unfold:

1) Fed flip-flops – data allows Powell to signal a policy pivot without reminding markets of the 70s on-again-off-again FUBAR (not happening yet – The Fed desires this financial conditions tightening until inflation is on clear path towards target);

2) China stops playing “patty-cake” with negative RMB fixes (digitals at 7.00 in CNH gonna trade imminently, it seems) and instead TRULY eases with larger, more substantial stimulus and Credit pumping to improve fundamentals—but only without ZCS, which is stifling any chance at recovery; and / or

3) Japan (BoJ / MoF / FSA) caves and adjusts YCC or intervenes in Yen.

Analyzing each of the above, McElligott notes that the Timiraos piece this morning has enormous implications – because of his “Fed Whisperer” profile, it effectively now “locks in” a 75bps hike, as it renders “only” a 50bps hike as a DE FACTO “EASING,” where the financial conditions move off the back of “only” a 50bps hike would be massively counterproductive for the Fed’s “Tight FCI”goals (as Real Yields and USD would plummet, Credit Spreads gap tighten and Equities Vol would get crushed).

{kind=link}

So don’t hold your breath for Scenario 1 to stop the ‘pain’.

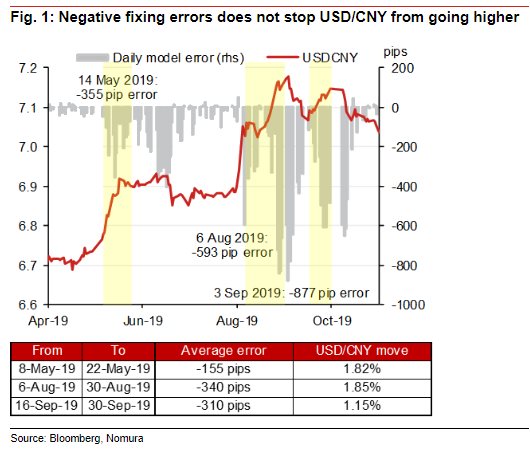

As far as China is concerned, especially regarding the current “weak” PBoC attempts to manage the RMB via the fix (as CNH sits at the 7.00 threshhold), Nomura FX Research’s Craig Chan notes:

Today’s fixing error of -505pips is the largest since October 2019. Although the market’s reaction was limited (there has been continuous negative errors since 25 August that we judge of significance; 10 sessions), it sustains concerns that the PBoC is acting against RMB depreciation.

Analyzing previous periods with significant consecutive negative errors (2019), negative errors do not stop USD/RMB from moving higher. An improvement in fundamentals is required (Figure 1).

{kind=link}

In May 2019, there were multiple errors of over -100pips, as RMB weakened on news that the US is raising tariffs on Chinese imports (Trump Tweet, 6 May; announcement, 10 May). Despite the errors, USD/CNY headed higher.

In August-October 2019, there were large negative errors regularly exceeding -500pips. Despite the -593pip error on 6 August, USD/CNY continued to head higher. It only started to decline from November 2019, as the phase one trade deal discussion started. This change in the environment eventually led to a multi-year outperformance of CNH versus USD and on a basket basis.

Currently, the environment is not conducive for RMB, and we reiterate our view to be long USD/CNH (we believe a break above 7.0 is imminent; year-end target: 7.2).

Therefore – don’t expect China to bailout your NFLX calls anytime soon.

And so finally, across the ocean to Japan, global market stress is particularly evident in Asian FX in recent days with The Asian Dollar Index is melting down to fresh 19 year lows in standard crisis form…

{kind=link}

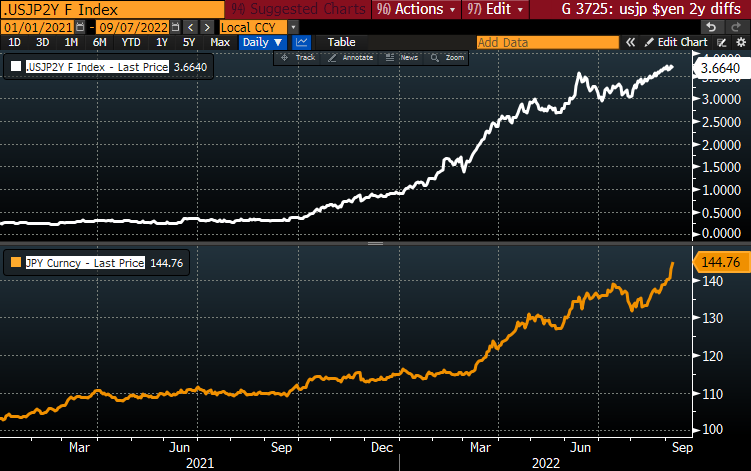

And we currently see $Yen now accelerating higher again towards the 145 level (!), despite FinMin Suzuki stepping-up comms – using the phrase “one-sided” for the first time since 2018.

McElligott notes that rate-differentials remain a large part of the story…

{kind=link}

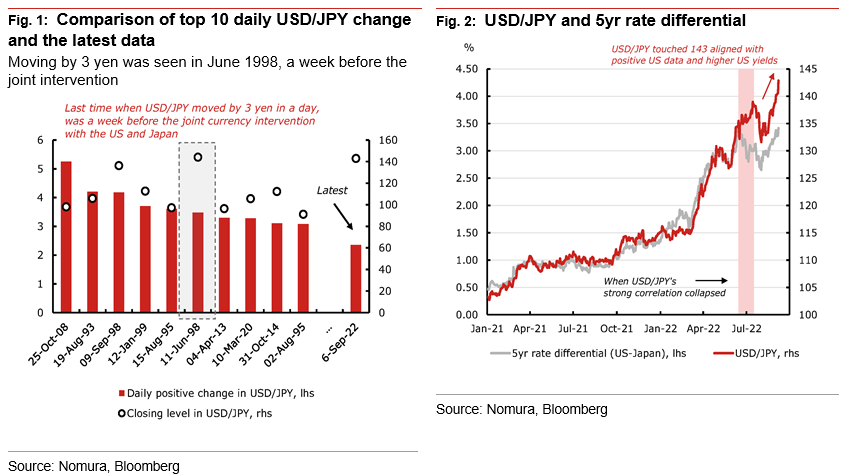

Technically speaking, the long-term view remains for a rise towards 180 as JPY resolves higher from the multi-decade base. Nearer-term, the rise is nearing the 1998 high at 147.66 and this could invite a pause to the rally.

{kind=link}

Regarding the Yen weakness and intervention / policy-adjustment risk (as $Yen pushes towards 145 in another 2 yen 1d move), Nomura FX Research’s Goto-San notes that we are now approaching the level that prompted a joint currency intervention by the US and Japan in June 1998.

However, based on verbal jawboning yesterday, we do not think JPY buying intervention is likely in the near term. We do not expect the BOJ to adjust its monetary policy at the September meeting due to JPY weakness as well.

{kind=link}

We will monitor the reaction of policymakers to the acceleration of JPY weakness but, in the near term, if there are no changes in policymakers’ stance, the risk of USD/JPY reaching 145 remains.

Fed’s Chair Powell’s speech this Thursday, as well as US CPI next week, are key event risks. Into year-end, we still expect the USD/JPY appreciation trend to inflect and weaken towards 130.

So – Japan is not expected to save the world here any times soon either.

That’s three strikes against any short-term relief from tightening global financial conditions and McElligott warns that CTA- and options-driven acceleration- and reversal- points are critical to understand as the speed of macro movements accelerates.

Tyler Durden

Wed, 09/07/2022 – 14:40