42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

“Very Crooked Numbers”: Biden Admin Accused Of Fabricating Low Gas Demand Data To Hammer Price Of Oil

Something very odd is taking place in the oil market: on one hand, when it comes to physical, buyers can’t seem to get enough: as we noted earlier Saudi prices for Asian buyers just hit a new record high, a clear indicator of relentless demand for physical oil no matter the price…

{kind=link}

… and yet at the same time, oil prices have tumbled today amid continued fears that demand for oil, and especially gasoline, will collapse when the US, Europe and the UK slumps into a recession… or already has.

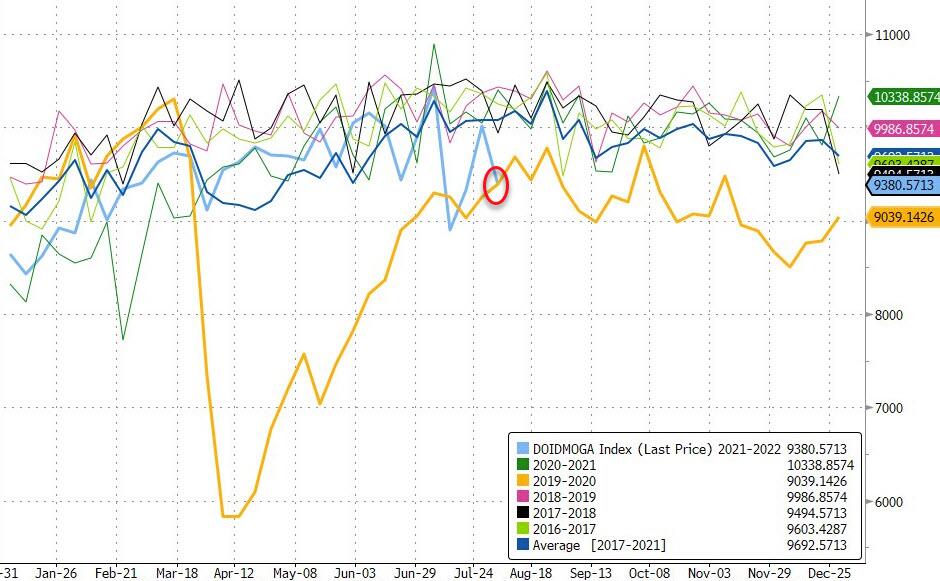

As our friends at ForexLive point out, the trigger behind today’s plunge in oil prices is gasoline demand, which as we noted yesterday, showed that for July, gasoline demand (on a trailing 4 week basis) slumped below 2020 levels.

{kind=link}

Intuitively, ForexLive cautions, “that doesn’t make sense. Yes, gasoline prices are much higher than 2020 but the world was in the midst of a pandemic and far more people were working from home in the summer of 2020.”

But the data is what it is and yesterday’s numbers were soft once again at 8540k. That was the main reason for the drop in oil yesterday and the decline through $90 today for the first time since the start of the Ukraine war. Next, ForexLive’s Adam Button runs through a quick list of factors laying out the arguments for both sides:

Why it might be true:

1) Elasticity: Gasoline is traditionally one of the least-elastic commodities — people need to drive. However there’s a limit and we may have it it in early July as gasoline cracks below out and US prices hit record highs. Around the July 4th weekend there were clear signs of demand destruction. Perhaps we hit a breaking point and drivers are cutting discretionary miles whereever possible.

2) Efficiency: There’s no doubt that cars are getting more efficient and people are switching to EVs and hybrids. That’s a secular trend that will weigh on gasoline demand in the long term. But compared to a year ago? The auto cycle is a long one and it will chip away at demand, but at a slow pace.

3) Flying more: The idea is that people and families are flying more this summer and driving less. Intuitively it makes sense. People were stuck driving to nearby locations for vaction for two years and now are branching out further. We’ve all see the nightmares at airports and flying is as busy as ever. Is that killing driving demand? Possibly but given that so much of driving is commuting and errands, it’s hardly believable that it could account for a 10% decline in demand.

4) Running on empty: According to GasBuddy, US retail gasoline prices have now fallen for 49 straight days. Following the gasoline price shock in late June, we could be seeing a behaviour shift in drivers where they are waiting longer to fill up gas tanks. That has been the right move for the past seven weeks and the drawdown in collective gas tanks could temporarily be masking demand.

5) Commercial pumps: The EIA data measures commercial gasoline demand — so from gasoline stations rather than consumers — so similar to the above, we could be seeing gasoline stations running with less inventory. That makes sense because right now the value of inventory is falling daily. Again, this would only be masking demand.

6) A sign of recession: All the talk of recession may have people cutting back on driving and spending. We’ve heard from Visa lately that’s not the case but weekly gasoline demand is some of the most up-to-date data out there. But if gasoline demand is falling this rapidly, what does it say about the rest of the economy?

7) Price is falling: Both crude and gasoline prices are falling and today oil is at the lowest since February. Could implied gasoline demand data really be fooling the market? There are reports on physical tightness and paper crude could be liquidating but I have a hard time believing that US demand figures are a major reason for oil weakness.

Why it might not be true:

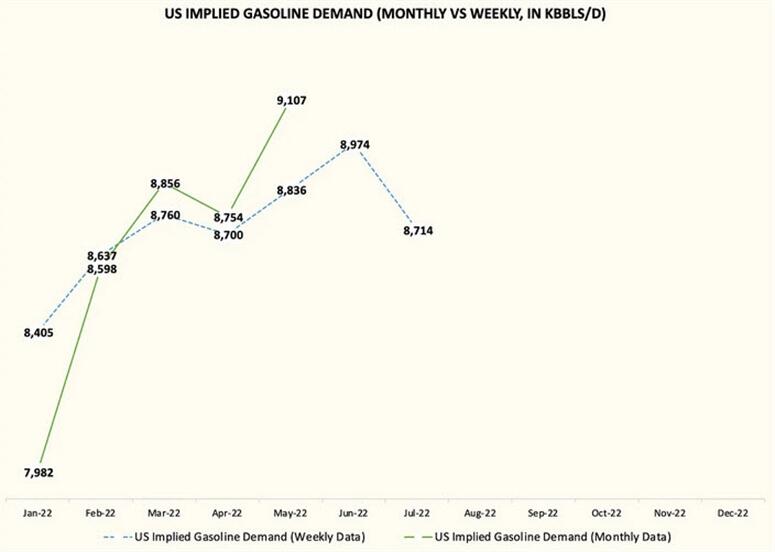

1) EIA data is subject to major revisions: The EIA does its best to get out petroleum data weekly but it’s a tough job and subject to all kinds of assumptions. HFI Reserach notes that the data is subject to big revisions when the month numbers are finally released. So traders may be simply looking at bad data that will be adjusted.

{kind=link}

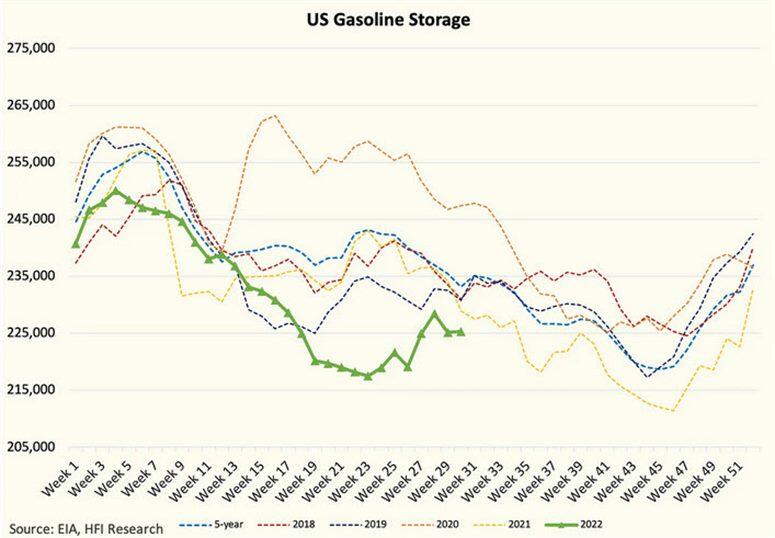

2) US gasoline storage remains at a five year low: Given cracks and pressure on to boost gasoline output, refiners have been working hard this summer. Combined with supposed lower demand, inventories should be moving up rapidly. Despite some progress, inventories are basically flat in the last month and still at five-year lows. This is another HFI chart and their explanation is well-worth reading.

{kind=link}

3) Refiners aren’t seeing a slowdown: US refining giant Valero was asked about falling gasoline demand last week and Gary Simmons, Chief Commercial Officer, had this to say: “I can tell you, through our wholesale channel there is really no indication of any demand destruction… In June, we actually set sales records. We read a lot about demand destruction and mobility data showing in that range of 3% to 5% demand destruction. Again, we’re not seeing it in our system.”

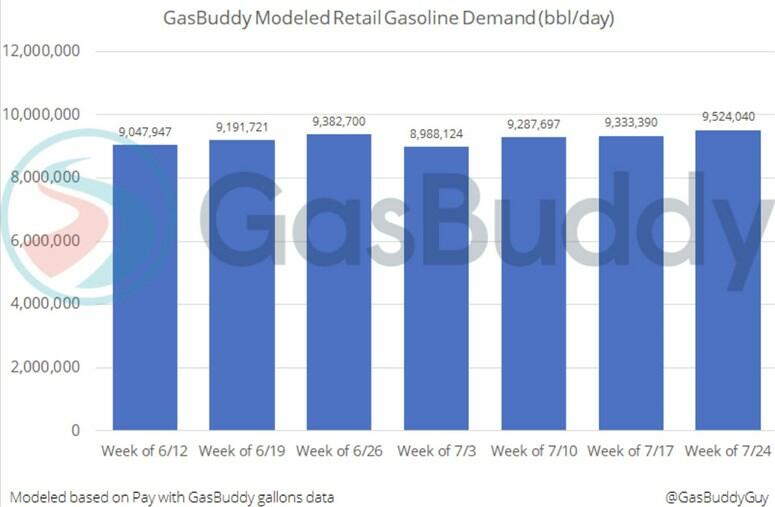

4) Alternate data doesn’t line up: GasBuddy tracks retail gasoline demand at the pumps in the US and they showed a 2% rise in gasoline demand last week while the EIA showed a 7.6% drop. Morevoer, last week was the strongest demand of the year from GasBuddy.

{kind=link}

Another data point shows vehicle miles traveled from the US Federal Highway Administration. While it’s only though May, it shows vehicle miles traveled up materially year-over-year through May. We’ll get the June data in the middle of this month.

{kind=link}

Conspiracy: Some are have gone so far as to accuse the Biden administration of explicitly “cooking the numbers” to depress the price of oil. As a reminder, in late-June the EIA shut down reporting for several weeks, supposedly due to a server malfunction; however since they have returned, the gasoline demand data has been consistently bad. “Maybe there’s an issue with reporting or maybe it’s a conspiracy”, according to ForexLive.

{kind=link}

But it’s not just same anonymous twitter randos screaming foul: last week Bank of America energy strategist Doug Legate published a note (available to pro subs in the usual place) titled the “fall of gasoline demand appears grossly exaggerated” in which he noted that last week we finally got the post July 4th rebound he suggested could follow the 4th of July holiday. “For the week ending July 22nd, implied gasoline demand rebounded to 9.2 million b/d – a 1 million b/d increase vs the last two week average, and the second highest level of 2022.” Curiously, right after that, however, we got a steep drop.

So steep, in fact, that Piper Sandler global energy strategist at Piper Sandler, yesterday called the data “crooked”:

“What is more bearish to the market is this notion that gasoline demand is falling away; we think that’s a very mistaken notion based on very crooked numbers from the [DOE] weekly data set... The way that the numbers are computed leaves significant room for error. We are supposed to believe that in July, in the middle of driving season we are only using 8.6 million barrels per day. That would be down half a million barrels a day from May of this year; that would be below the Covid low of 2020. So we ask all the refiners, we ask all the retailers, we ask everybody that reported earnings this season. Every single one of them tells you that their sales are not down materially from even pre-covid days. Some report record high sales.”

If there is indeed “crooked” data, it comes at a strategic time: just as Brent tumbled below the 200DMA, in the process triggering systematic sell orders which push the notoriously momentum-chasing also community short the commodity.

Alas, as Adam Button concludes, “at the end of the day traders have to trade what’s in front of them. Right now it’s a crude chart that’s breaking support after a major period of consolidation — that’s not good. The calls for a recession are growing louder crude demand has a long history of following global growth. There are supply factors that will eventually be bullish — like the SPR releases ending in October — but that’s months away and OPEC is still adding some barrels.”

Finally, for those wondering to what lengths the Biden admin would be willing to go to hammer the price of oil, and gas at the pump, sharply lower ahead of the midterms, we remind you what is going on with the US strategic midterm petroleum reserve which has been drained by 110 million barrels since the start of the Ukraine war (with much of it going to China) to levels last seen in May 1985.

{kind=link}

One better hope the US doesn’t encounter a real emergency in the next few weeks, beyond more than just Biden’s approval rating hitting an all time low.

Tyler Durden

Thu, 08/04/2022 – 14:03