42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Rescue-Fund Idea Floated To Stop Mortgage Crisis

By George Lei, Bloomberg Markets Live reporter and analyst

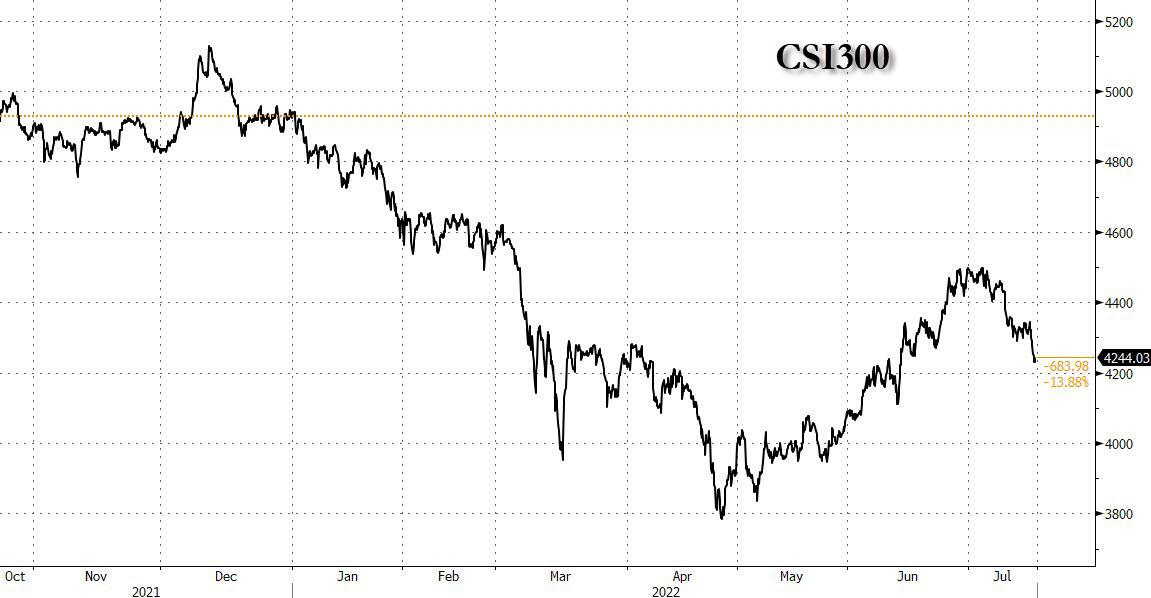

The Chinese stock market suffered its biggest weekly loss in three months, with the benchmark CSI 300 index sinking more than 4%. Real estate and banking risks soured sentiment and surging Covid cases made matters worse.

{kind=link}

Last week, housing ministry officials met with financial regulators and major Chinese banks to discuss lending matters. The government also censored crowd-sourced documents tallying the number of mortgage boycotts across the country. Markets, however, expect much more. Swift policy responses coordinated from Beijing are urgently needed to prevent bigger market rout.

Knee-jerk reactions from local authorities may be to tighten oversight of escrow accounts for new home sales, and for banking regulators to raise mortgage standards. After all, a key reason for the mortgage boycotts is that developers diverted homeowner payments for other purposes. Now that many developers are facing financing difficulties, construction on those unfinished homes stalled.

Such moves make perfect sense in isolation. But they might cause more troubles nationwide if implemented together. More money in escrow means less for developers, which could “lead to a sustained slowdown in housing market activity and more developer defaults,” according to a JPMorgan client note written by Tingting Ge, Haibin Zhu and Grace Ng on Friday. Relaxation of escrow management, on the other hand, would create the risk of embezzlement that could hurt more homebuyers.

Nomura also expects “stricter control over presale escrow accounts” that would “hurt sales demand further,” credit desk analyst Iris Chen said in a note on Thursday. Mortgage issuance may also face a stricter approval process that could slow down cash collection and add pressure to developers’ liquidity.

The mortgage boycott news, paradoxically, reduced concerns that accommodative macro policies might be pulled back, according to a client note from Goldman Sachs. Analysts Maggie Wei, Hui Shan and Lisheng Wang talked with clients including asset managers, private equity and hedge funds in Beijing and Shanghai. They found that domestic investors have high expectations for additional fiscal measures, such as more government bond issuance or further financial support by policy banks.

Monetary easing alone cannot provide a quick fix to property sector problems, Xu Gao, chief economist at Bank of China International told local media. He floated the idea of a 1 trillion yuan ($148 billion) relief fund to buy non-controlling equity stakes in troubled developers. Once the builders are adequately capitalized with state-backed money, banks will be more willing to lend and the public will feel more assured of their new home purchases.

There are plenty of precedents for such rescue facilities. In 2008-09, the US Treasury spent about $250 billion to stabilize banks and $46 billion to help struggling families avoid foreclosure under the Troubled Assets Relief Program. Premier Li Keqiang said in March that Beijing plans to set up a fund for ensuring financial stability without giving more details.

Now, it looks like homeowners, banks and developers all need some lifeline to see through the mortgage crisis. Policy makers in the very top will need to act swiftly and decisively. The consequences of inaction, or a piecemeal, uncoordinated approach, can be very costly.

Tyler Durden

Sun, 07/17/2022 – 22:47