42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

People Are Now Resorting To Micro-Loans To Afford Groceries & Gas

Two months ago, President Biden read off of a teleprompter: “I’ve built a strong ec- — we’ve built a strong economy with a strong job market.”

Two months later, and cash-strapped Americans are using micro-loans to afford gas and groceries amid crippling inflation.

{kind=link}

As Bloomberg reports, Swedish fintech company Klarna Bank – whose bread & butter has been loans for smartphones and other consumer electronics – has seen a flood of applications for staples such as food and gas. They provide interest-free loans that allow people to spread payments out over multiple installments, and makes money charging retailers a small per-transaction fee, and from interest on longer-term loans.

{kind=link}

“I noticed that I could buy essentials with it, and not have to pay everything up front. And it wouldn’t affect my pocket as much,” said Linda Cruz, a 37-year-old mother of four from a small town near San Antonio, Texas.

Linda Cruz, a mother of four from a small town near San Antonio, Texas, started out using Klarna’s interest-free loans for occasional, large purchases — like a new air conditioning unit after hers died during a heat wave last summer. But as prices started to rise for essentials, she started using it for groceries, too.

Cruz, 37, a bail bonds agent and her family’s sole earner, is paid bi-weekly and said Klarna is a useful budgeting tool, letting her take care of her bills when she gets a paycheck. -Bloomberg

Meanwhile, Klarna just closed an $800m round of financing at a $6.7bn post-money valuation – a fraction of the nearly $46 billion valuation it achieved last year – so perhaps this Bloomberg article is simply marketing a new niche for the 17-year-old lender that says it’s “embraced the shift in the way people use its credit.”

Klarna, run by co-founder and Chief Executive Officer Sebastian Siemiatkowski, has struck partnerships with gas companies such as Chevron Corp. and developed an app that can be used in physical stores at retailers, like Walmart Inc. and Target Corp., as it hunts for new users. But interest rates for its own debt are rising and Klarna’s burning through hundreds of millions of dollars per quarter, making the company more vulnerable to defaults from customers living paycheck-to-paycheck.

“This puts pressure on the Klarna model,” according to Warwick Business School professor John Colley, who adds that as the disposable wealth of the company’s users shrinks, “Klarna will be sat there with substantial bad-debt risks. Their customer base is likely to be sub prime anyway.“

I mean, this is performance art pic.twitter.com/NHtOHomNg7

— Peter Thal Larsen (@peter_tl) July 11, 2022

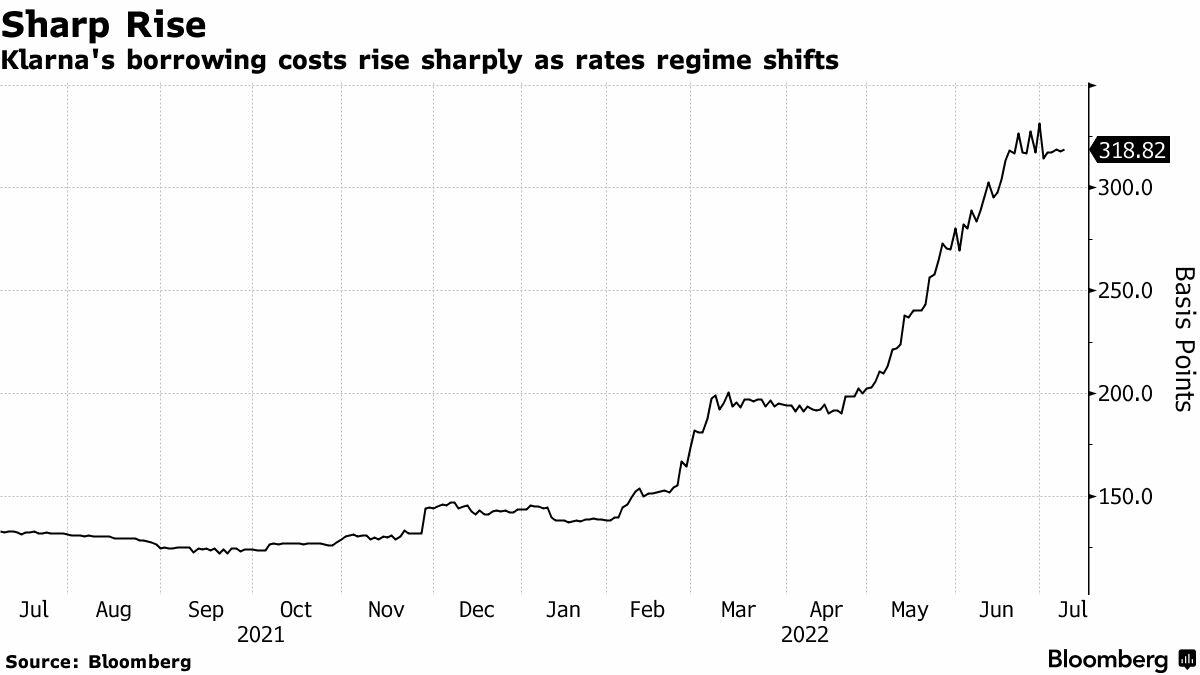

According to the report, the drop in valuation tracks with the meltdown in capital markets – though notes that Klarna is “particularly vulnerable because higher interest rates, aimed at curbing inflation, boost its own borrowing costs.”

While Klarna doesn’t disclose its default rate, the company evaluates customers’ ability to repay on every transaction and losses are consistently less than 1%, a spokesperson said.

Klarna’s cost of borrowing in the open market has risen sharply in the first half of 2022. A February 2024 floating rate bond has seen Klarna’s discount margin, a measure of the credit spread over benchmark borrowing rates, climb to 318 basis points. That pushed the company’s two-year borrowing cost above 4%, more than double what it was at the start of the year. -Bloomberg

A spokesperson told Bloomberg that their absolute credit losses are higher y/y due to a surge in new users.

{kind=link}

“The risk that you are building up is a debt problem that could be exacerbated by the cost-of-living crisis,” said Sue Anderson, an official with debt charity StepChange, which found along with Barclays bank that 36% of users say micro-loans have become more appealing amid the record inflation. (Ya think?)

“People don’t see it in the same way they see other types of borrowing,” Anderson continued, adding “It is marketed as interest-free, but that doesn’t mean it is risk free.”

Tyler Durden

Tue, 07/12/2022 – 06:55