42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Canary In The Car Mine: Repos From Auto Loans That Originated In 2020 And 2021 Are Skyrocketing

If you’re looking for proof that we’re already in the midst of a meaningful deleveraging, look no further than car repos.

In fact, the industry is a “underappreciated ticking time bomb”, according to Barron’s. One car dealer said this week that most loans on cars currently being repossessed originated during 2020 and 2021 – a trend that differs from the norm, when origination dates are usually scattered.

“Many of the loans were extended to buyers who had temporary pops in income during the pandemic,” the dealer, who has been in the business for 20 years, told Barron’s. The monthly incomes of many who took on the loans have fallen “sometimes by half” now that stimulus programs have ended, the report says.

Consumers’ incomes were temporarily high as a result of debt forbearance, pandemic stimulus checks, enhanced unemployment benefits and PPP loans, the report says. The auto dealer says he bought a Bentley, McLaren and two Aston Martins from two buyers, now in default, who used PPP money for down payments.

“Everybody thought the free gravy train would never end,” he said. He told Barron’s he has “never seen so many people making $2,500 a month owing $1,000 a month in car payments.”

{kind=link}

“The idea that the economy is strong? Anyone who is actually doing business sees things are not strong. We had a housing bubble in 2008, and now we have an auto bubble,” he continued. He guessed, based on data he has seen from banks, that “subprime repos have nearly doubled since 2020, to around 11% on average”.

Normally, about 2% of prime loans wind up being repossessed. That number now stands at about 4%. Continuing data on repos is difficult to find, the industry insider said: “A lot of the banks—they’re smart. They control the market, like diamonds. As repos pour in, they only release them so often.”

“The bubble is beginning to show signs of bursting soon,” said Pamela Foohey, law professor at Cardozo School of Law at Yeshiva University, who was one of the first to warn about trouble in the sector back in 2021.

Auto debt is now about 10% of all total consumer debt, rising $87 billion for the year ended March 2022, to a total of $1.47 trillion.

And as Danielle DiMartino Booth, CEO of Quill Intelligence, correctly points out in the article, automobile repos are usually the canary in the coalmine when it comes to economic trouble on the horizon.

Recall, back in May we noted when cracks in the auto market started to appear. At the time, the WSJ reported that millions of Americans with subpar low credit scores were falling behind on paying their credit cards and automobile and personal loans.

At the time, we called it “an ominous sign the ‘strong consumer’ narrative is cracking.”

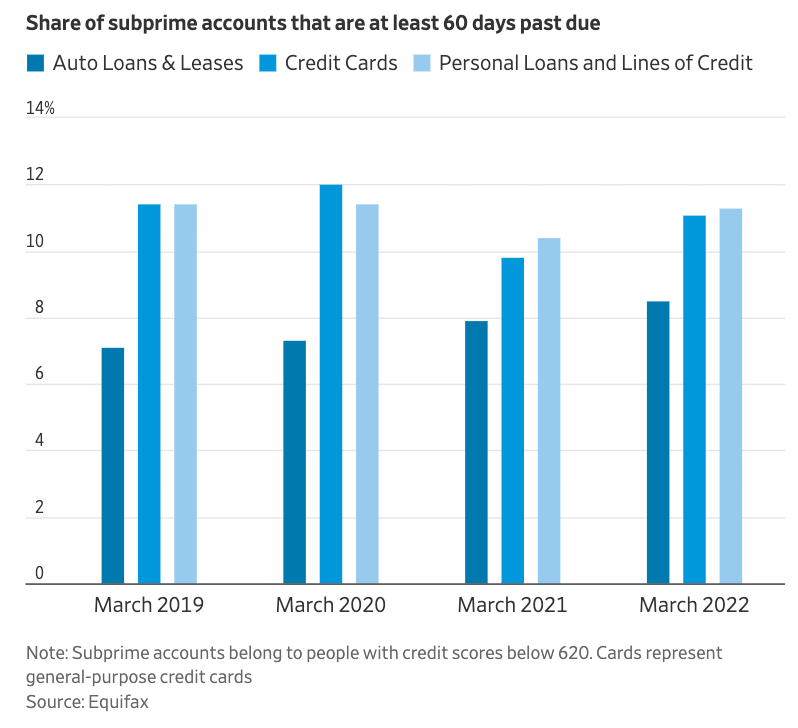

Data from credit-reporting firm Equifax Inc in May had already started to show a rise in the share of 60-day delinquencies for subprime credit cards and personal loans. Those delinquencies hit an eight-month high in March, nearing levels not seen since before the virus pandemic.

Equifax’s data also showed subprime car loans and leases soared to a record-high in February. The data goes back to 2007.

{kind=link}

Tyler Durden

Tue, 07/12/2022 – 14:40