42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Goldman: ‘Defensive Rotation’ From Stocks To Bonds Will Make Gold Shine Again

A week ago, we laid out why Goldman Sachs’ had increased its target price for gold to $2500, suggesting pressure on the precious metal would ease as China’s “negative wealth effect” eased.

Since then prices for precious metals have tumbled…

{kind=link}

So what will be the catalysts for gold to shine again?

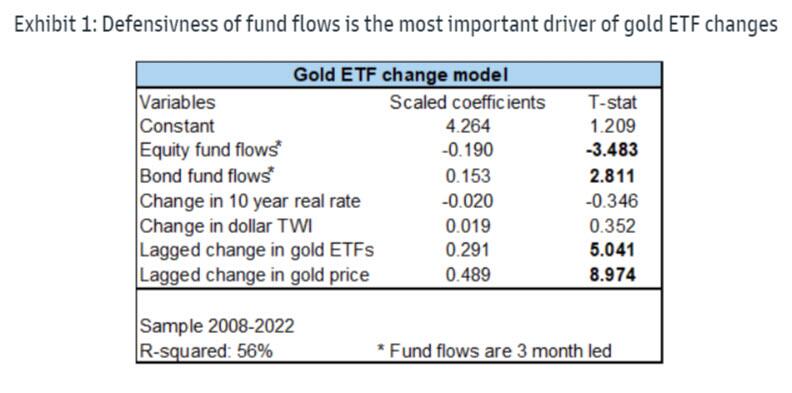

In his latest note, Goldman’s Mikhail Sprogis explains that for gold investment demand to build momentum there needs to be a defensive rotation out of equities into bonds.

Sprogis view gold prices through a ‘Fear and Wealth’ framework, where ‘Fear’ drives investment demand in DMs and ‘Wealth’ drives consumer demand in major EM gold consumers.

US recession risk and central bank (CB) policy tend to be the best proxies for Fear, while the dollar GDP of gold consumers is the best way to track the Wealth effect.

Thus, so far this year gold investment demand remains split between hawkish CBs who are committed to bringing inflation down, a negative force for gold prices, and high recession worries, a positive force.

The future direction of gold investment demand will be determined by the interplay of Fed hawkishness and recession fears, in Goldman’s view.

If recession fears persist while the pace of Fed hikes slows down due to a normalization of inflation, then gold investment demand should finally manage to build a bullish momentum. We observed a similar dynamic at the start of the year, when growth and inflation worries emerged but it was unclear how hawkish the CBs’ response would be.

If, however, recession fears were to moderate due to a resilience of US growth while sticky inflation forces the Fed to continue to hike, then we are likely to see a material rotation out of gold ETFs.

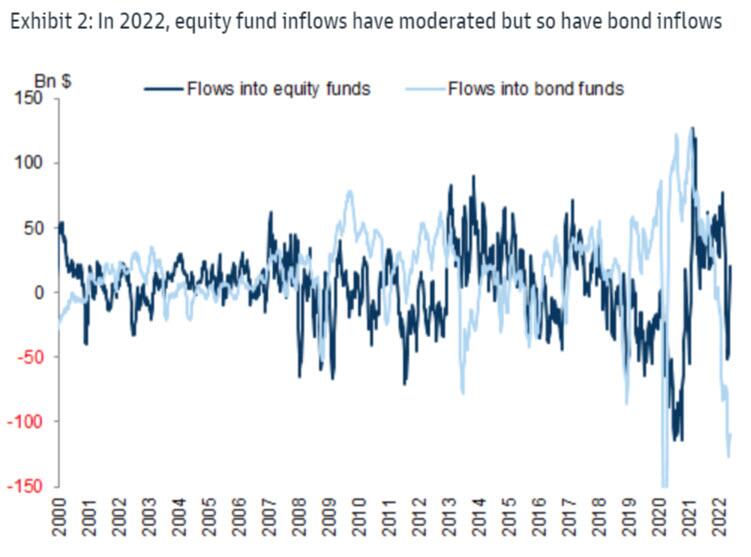

This dual nature of gold investment demand can be seen in the relationship between gold ETF flows and flows into bonds and equity funds.

{kind=link}

Flows into gold ETFs tend to be positively linked to inflows into safe bond funds and negatively correlated to flows into risky equity funds.

{kind=link}

Goldman concludes:

All in all, we believe that the moderation of inflation rates can shift the market focus from continued tightening and towards recession risk.

This should be positive for gold, in our view, as it would relieve pressure from the continued rising dollar and rates but keep the support from high recession fears.

We therefore expect gold to begin to perform as the market sees more credible indications that the Fed hiking pace is moderating and there is a rotation out of equities into bonds.

As a reminder, Baupost’s Seth Klarman said in his latest note to investors that:

“I’m a fan of gold. I think gold’s valuable in a crisis.”

“The market has come to believe in an omniscient Federal Reserve, and it’s no such thing. These guys don’t really know what they’re doing in any deep way. It’s a giant financial experiment, and we’re at the mercy of their experiment that maybe is right now in the process of going wrong, so God help us.”

It seems The Fed’s omniscience is about to be tested…

Tyler Durden

Sat, 07/09/2022 – 15:00