42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

“The Fed Now Has Good Reason To Surprise Markets”: Barclays Is First Bank To Call For 75bps Next Week

With Wall Street still stunned at today’s blistering red-hot CPI, and with 2Y yields blowing out almost 20bps today, rising above 3.00%, the highest since 2008 (right around the time Lehman was sacrificed for the greater good) broad-based price pressures, with little indication that these have peaked, banks are starting to break ranks with the Fed-imposed consensus, and are predicting that the Fed will shock markets next week when it will hike more than it has guided.

{kind=link}

As Barclays rates strategist Jonathan Millar writes, he is “getting ahead of the curve: We expect a 75bp hike at the June meeting.”

Below we excerpt from his note (available to pro subscribers)

As markets absorb today’s CPI print, the US yield curve is bear-flattening hard, with 2s up 13-14bp at the time of writing [ZH; 19bps now]. But market expectations regarding the June meeting have been less volatile, with investors pricing in just over 50bp.

We disagree. We think the US central bank now has good reason to surprise markets by hiking more aggressively than expected in June. We realize it is a close call and that it could play out in either June or July. But we are changing our forecast to call for a 75bp hike on June 15. We have also lifted our forecast for the terminal rate by 25bp, to 3.00-3.25%, in early 2023.

There are a few drivers of our non-consensus call.

First are May’s very firm prints for headline CPI (+1.0% m/m) and core (+0.6% m/m). It is not just the headline print; if all of that came from energy, we would be inclined to look past it. But everything in this report was strong, and turning stronger. Used vehicle prices changed direction and rose again; airlines added yet one more hefty surcharge ;despite a large jump in the prior month;and, worryingly, rent inflation accelerated to 0.6% m/m. In other words, don’t blame energy; this report shows inflation pressures not just accelerating, but also broadening. Second are medium-term inflation expectations. 5y5y CPI swaps are not yet at the absolute highs of the year, but they are close. Moreover, other gauges of medium-term inflation expectations are also showing signs that the Fed may be losing inflation-fighting credibility, with the 5-10y inflation expectation component of the University of Michigan Consumer Sentiment Survey rising 0.3pp, to 3.3%, in the preliminary June survey – just off a 27y high set in spring 2008. This is despite global growth forecasts decreasing aggressively in recent months, a very significant risk-off and tightening of financial conditions, and with parts of China being offline for much of Q2. And of course, there is the history of the past six months. In virtually every major economy (even Japan), inflation prints have surprised over and over to the upside. Then surprised to the upside some more. Central banks, led by the Fed, have pivoted hard, yet have found themselves behind as the spot inflation data blow past their pivot. Again and again.

The tricky part behind going 75bp, of course, is that the Fed then has to bat down expectations of 75bp hikes at subsequent meetings. But that messaging hurdle was one that it also faced when it essentially committed to 50bp for at least a few meetings, and that did not stop it from making this commitment. It is also possible that a number of things suddenly fall into place over the next few months. Auto dealer margins could come down sharply, the inventory drag that retailers are complaining about could show up in large discounts of goods prices, and signs of moderation in wages in recent months (the one saving grace on the inflation side) could become more visible. Even on rents, housing activity has slowed hard, and at some point, rents could well moderate, and quickly. And if all of these developments occur, both markets and the Fed will change their mind about the fed funds path. But what if they don’t? Moreover, none of this hoped-for moderation will be visible by June 15. Even next week’s retail sales number will be available only on the same day as the Fed meeting, and any weakness there is unlikely to play a major role in the next policy decision.

As Barclays concludes, historically, the Fed has avoided surprising markets – say, by going 75bps when it is not priced in because as Powell himself has said, he will only hike 50bps. But next week, Barclays feels, “is likely to be one of the exceptions. The Fed should want to surprise the markets by being more hawkish than expected, given the magnitude of upside surprises in recent inflation data.” That’s why the bank thinks “the likelihood of 75bp in either June or July is high and that the June meeting is most likely.”

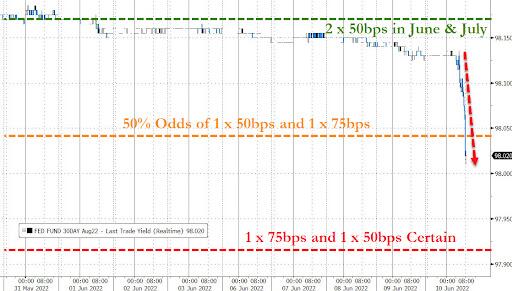

It appears that Barclays is on to something because moments ago, the market implied odds of a 75bps rate hike next week just rose to 55%…

{kind=link}

… with Fed-dated OIS now pricing in 163bp of additional hikes over the next three policy meetings, up from 145bp priced in the lead up to the May CPI data. And with 114bp priced in; further out, there are 232bp of additional hikes priced into the December FOMC meetings, up from 210bp priced before CPI data.

Tyler Durden

Fri, 06/10/2022 – 11:33