42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Did CPI Just Peak?

A lot has been said about today’s “extraordinary“, scorching CPI print which we discussed on at least two occasions (here and here), but the biggest outstanding question is whether today’s blowout print was the top (despite Jeff Gundlach predicting on his latest DoubleLine call that inflation may hit 10%). Well, as we noted earlier, according to a number of Wall Street banks, today’s scorching number was indeed the peak of the inflation wave, and over the past few hours many more have joined them including Goldman…

{kind=link}

… Deutsche Bank…

{kind=link}

… and JPMorgan.

{kind=link}

So what’s behind these bold declarations? After all, the past year is littered with one after another wrong conclusion by Wall Street (and Fed) bankers that inflation was either transitory or couldn’t rise any higher. Is this time any different.

Let’s take a look at the facts:

First, there is the base effect, and indeed after March things tend to normalize due to the two-year anniversary of the post-covid collapse which troughed in March 2020 and has been ‘renormalizing’ ever since.

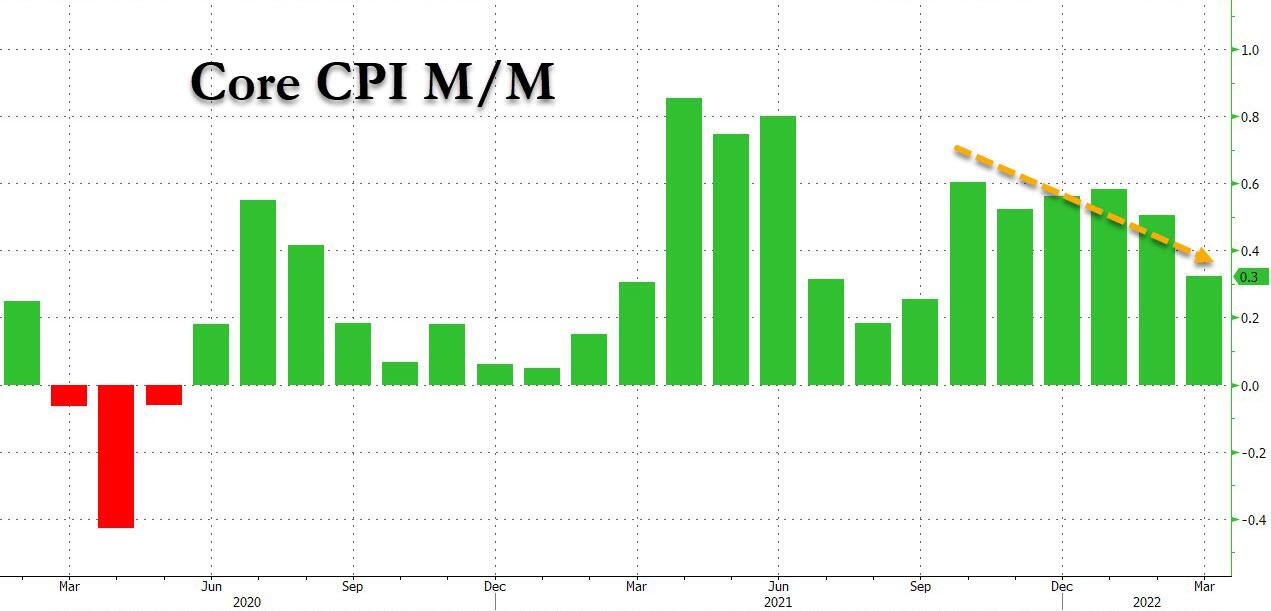

Second, at 0.3% M/M, core CPI not only missed expectations of 0.5%, but rose at the lowest level since September 2022.

{kind=link}

Third, there is the modest slowdown in the all important OER, shelter and rent space: in March, OER and rents of primary residence both came in at 0.43% mom, cooling slightly from February. And even if on a Y/Y basis, shelter inflation printed at the highest level since 1991, it is likely that we have hit the peak for the sequential rate, although we will surely have elevated readings going forward for quite some time.

{kind=link}

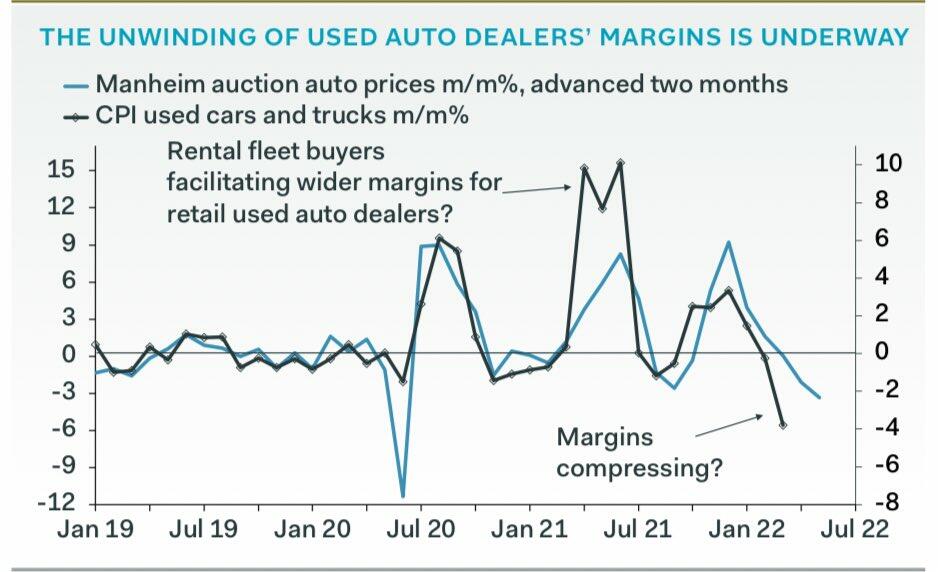

Fourth, car prices: last Friday we asked “Are Used Car Prices About To Peak For Real This Time?” and today the BLS came close to giving us the answer, when the index for used cars and trucks fell 3.8% in March, its second consecutive monthly decline after a series of large increases, and singlehandedly was responsible for subtracting 20bps from the core print (core would have risen 0.5%, in line with expectations otherwise).

{kind=link}

One can argue that the drop is only just starting, and Pantheon Macro does just that, repeating what we said this morning and writing that “plunging used vehicle prices explains the undershoot in the March core CPI; they have much further to fall. .. the potential for it to be a huge drag on core inflation over the remainder of this year is very real.”

{kind=link}

Picking up on this, Deutsche Bank writes that with vehicle inventories being rebuilt and wholesale used car inflation trending down, automobile prices should cease being a major contributor to inflation, at least in the near term, and the bank expects used cars to be another meaningful drag on the April core CPI print.

That said, there is a big footnote here, and as “the big short” Michael Burry pointed out, it is likely that the BLS may have figured out that in order to push inflation down it has to hammer car prices and that’s precisely what it plans to do next month when in addition to manipulating the artificially low OER series, the BLS is now taking aim the vehicle prices too.

CPI says housing costs rose 5.0% last 12mos. Wrong. CPI would be 12.0% using real-world NAR housing data. BLS has smoothed out housing numbers forever because home prices have been a problem forever. So next month they will start smoothing out vehicle prices. #problemsolved pic.twitter.com/KDdwADZgZi

— Cassandra B.C. (@michaeljburry) April 12, 2022

Fifth, while banks are always wrong, one voice which still carries some credibility is that of Jeffrey Gundlach and speaking to CNBC today, he said that “we are near peak inflation“, then again exactly one month ago he also predicted that inflation would hit 10% (and one year ago, he also said that inflation would peak in July 2021), so perhaps he isn’t the best authority on the matter either.

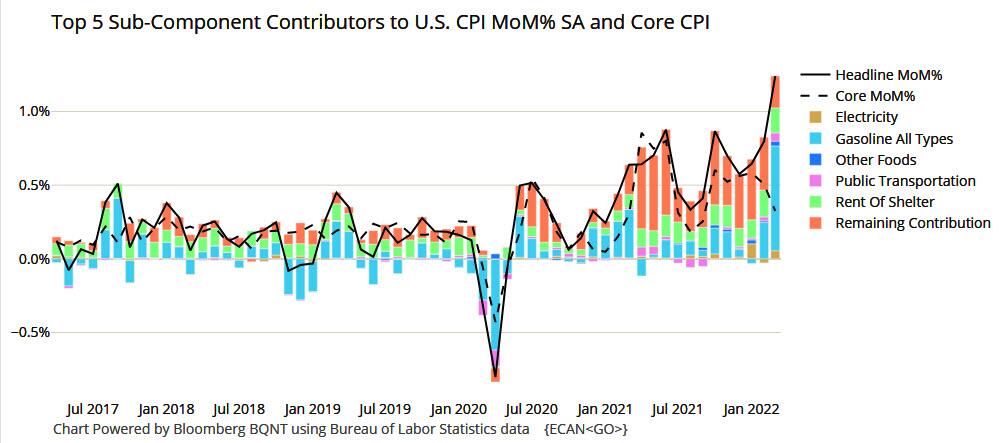

To be sure, there are various reasons to be skeptical that peak inflation is here. First, food and energy added significantly to the headline print, with the former growing 1% month-over-month for the second month in a row and the latter notching the second highest monthly gain in the series’ sixty-five year history (+11.0% vs. 13.5% in September 2005). While it is difficult to predict which way energy prices will head next, with the Biden admin making them the primary target of Democrat pre-midterm agenda even as the raging Ukraine war assures that commodities will remain very high for a long time, one thing is clear: food has yet to feel the impact given lagged pass-through and as Bank of America siad, is likely to remain hot throughout the year. In other words, while much of the covid-linked supply chain inflationary spike is fading, we are about to face an even bigger, Ukraine-war food inflation spike. Granted, this won’t hit core inflation as much, but try telling American households that high double-digit food inflation doesn’t count.

{kind=link}

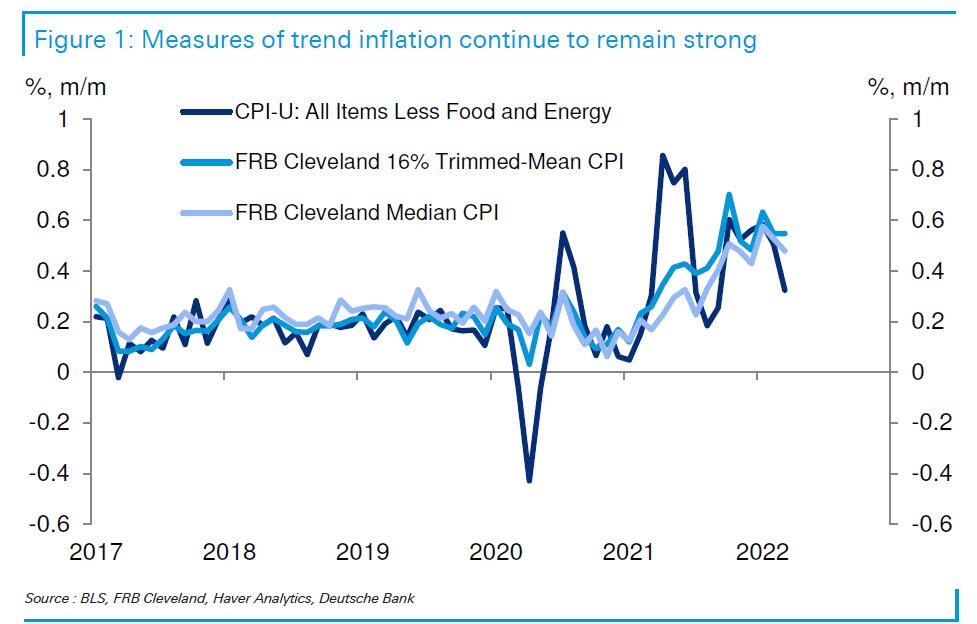

Another reason to be skeptical of calls for peak inflation is that as noted above, most of the impact from the downside outliers was a function of used cars and trucks. As such, alternative measures of trend inflation like the trimmed mean (+0.55%) and median (+0.48%) CPI came in significantly stronger than core. On a twelve month basis, both of these measures of underlying inflation continued to push higher. This is a continuation of the previous trend, which has seen a variety of measures of underlying inflation rising.

{kind=link}

Add to this that while used cares have finally dropped (and they also dropped last summer only to surge right after), household furnishing and supplies (+1.0%) and apparel (+0.6%) both posted outsized gains indicating that supply chains remain snarled. Given recent geopolitical developments, Deutsche Bank warns that a major risk is that further deterioration in supply chains could eventually begin to impact vehicle prices again, precisely what we warned about last week.

{kind=link}

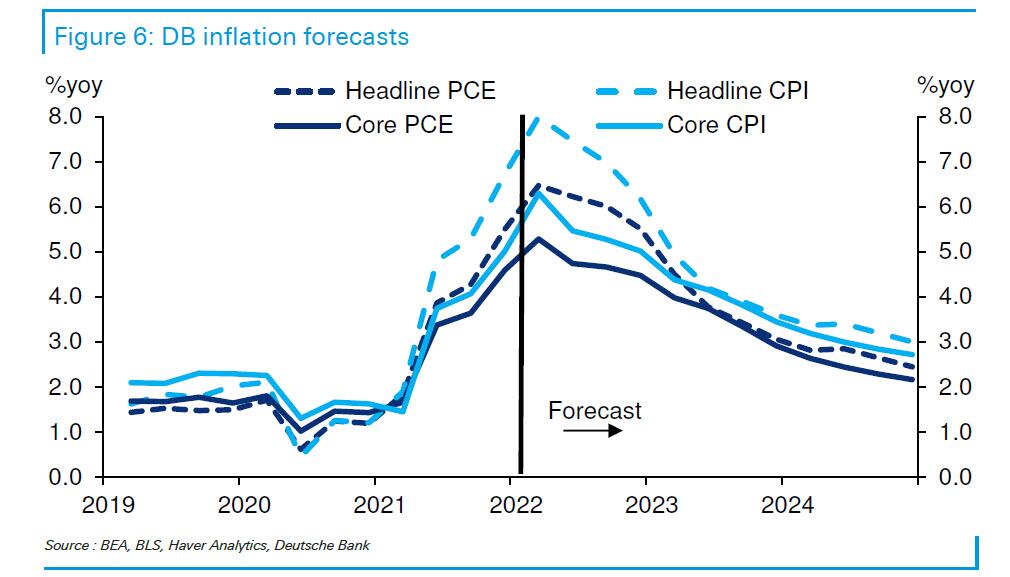

With both sides of the argument laid out, where do the banks stand? Well, as noted above, for better or worse they have decided to call peak inflation right here, right now, with DB writing that “our longer run view on core CPI remains steady, with inflation beginning to decline in the April data to end this year at 5.0% (Q4/Q4), 2023 at 3.4%, and 2024 at 2.7%. Food and energy inflation should serve to keep headline inflation above core, with the corresponding values for headline at 6.2%, 3.6%, and 3.0%, respectively.”

{kind=link}

And with both Goldman and JPM also jumping on the “peak inflation” bandwagon, all we now need is for central bankers to climb on board and to conclude that this time inflation – no longer transitory mind you – has finally peaked. That will be the clearest signal yet that a lengthy period of brutal stagflation is now inevitable.

Tyler Durden

Tue, 04/12/2022 – 22:25