42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

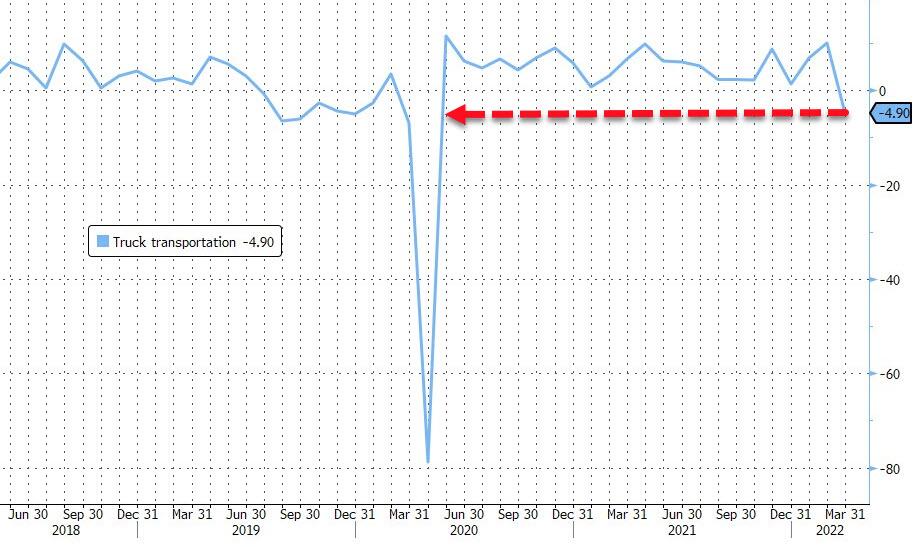

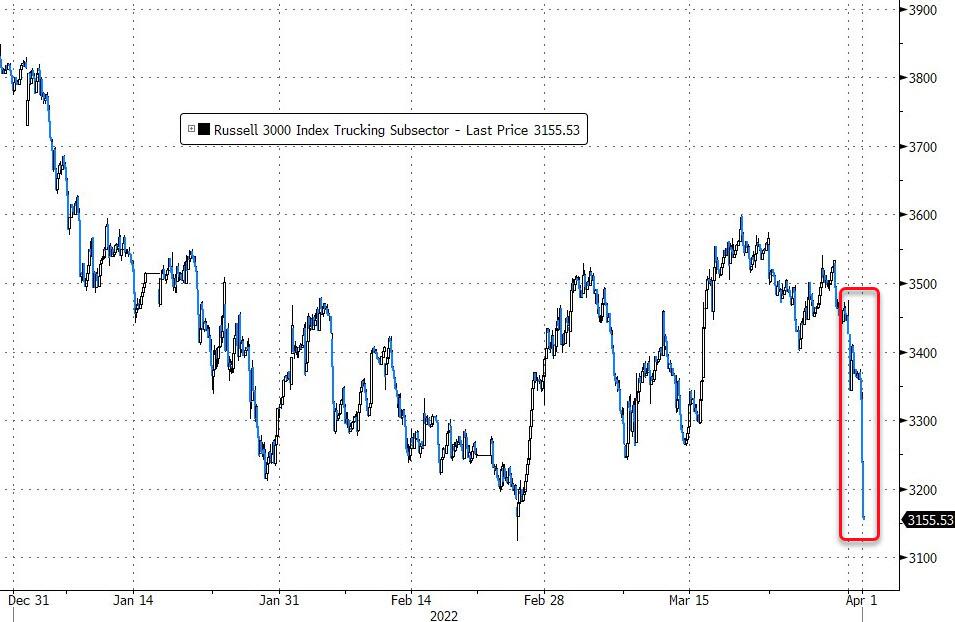

Trucker Stocks Plunge After First Post-COVID Job-Losses As Freight Recession Looms

Update (1040ET): Confirming the expectations of a freight recession explained below, US Truckers saw the first month of job losses in March since the COVID lockdowns…

{kind=link}

This helped spark a collapse in Trucker stocks, back to the lows of the year…

{kind=link}

* * *

As FreightWaves’ CEO Craig Fuller detailed earlier, a freight recession is imminent.

Last week, I published an article entitled “Just 3 years after 2019’s trucking bloodbath, another is on the way.”

{kind=link}

For anyone who lived through the trucking debacle of 2019 – when carrier after carrier suddenly shut their doors – the thought of experiencing that again is truly frightening. After all, we lost some very large carriers during that period , including Celadon, Falcon and NEMF, just to name a few. In addition, we lost thousands of small and mid-sized trucking companies. In addition, major 3PLs conducted aggressive reductions in force.

A Celadon truck sits after the company’s shutdown

{kind=link}

The article stoked controversy. Some disagreed with my call and voiced it directly to FreightWaves or on social media.

First off, different opinions and disagreements are part of a healthy market. When I started FreightWaves in 2017, the goal was to create transparency in the freight market, much like you see in the financial markets. In order to accomplish transparency, there needs to be an open dialogue between those of us interested in the direction of the freight market.

When FreightWaves was just beginning, I was told by an editor at a major publication (who has been covering supply chains for many decades) that trucking rates were not volatile and they barely moved. I’m still not sure why he believed that, but I suspect he thinks differently now.

Trucking has always been volatile. It is one of the most fragmented markets on the planet, with few barriers to entry. Carriers come and go. Booms are followed by busts. The typical trucking cycle is three years and usually what kills it is oversupply – too many trucks chasing high-paying spot freight and high load volumes.

The problem is that capacity expansion always continues well past the peak and can even continue for a time after the market has entered a recession. In the bloodbath of 2019, the peak of the market took place during the second quarter of 2018. However, it wasn’t until September 2019 that the number of new entrants into the trucking market peaked.

At FreightWaves, our business is benchmarking, analyzing, monitoring and forecasting freight markets. And much like financial market information services providers, having the freshest insights into the market is incredibly important to our success.

FreightWaves tends to call inflection points much earlier than other industry observers. It’s a big part of the value we provide our audience and clients.

On February 27, 2020, we warned that the freight market was about to see a massive disruption due to COVID, and that it wasn’t factored into historical data or market sentiment. This was two weeks before the “NBA and NHL moments,” when those sports leagues called off their seasons. At that point, most believed that the U.S. would avoid disruptions from COVID. Unfortunately, two weeks later, the worst health crisis in modern American history began.

That’s the disadvantage of looking strictly at historical data and shows why having the most up-to-date data in the market is critical, particularly in a market as volatile as the trucking freight market.

As I wrote back then: “The coronavirus is a black swan event not reflected in historical data. These unforeseen events make it clear why near-time data is crucial for freight operations.”

It turned out that FreightWaves’ analysis was correct and anyone relying on historical data or data without context was going to be wrong.

Throughout the COVID disruption, FreightWaves continued to provide real-time data and to analyze the trucking market with the freshest perspective on what was happening. This real-time analysis provided insights that were unmatched and unlike any in the history of the freight industry – government agencies, financial institutions, multinational corporations, and transportation providers all relied on FreightWaves to keep them informed during a confusing, dynamic situation.

In the trough of the COVID shutdown, we called for a freight bull market – and nailed it

On April 15, 2020, I wrote the blog post “GOOD NEWS: THE FREIGHT MARKET IS ABOUT TO TURN UP.” At the time, the global economy had just shut down, most states had implemented drastic measures to contain COVID and unemployment hit new records. It was a dark and scary time, but I was bullish that the freight market was about to accelerate.

As I wrote at the time:

“So here is the good news. The contract trucking market seems to be bottoming out. The declines we saw in trucking tenders seem to be leveling off and there are signs of a bottom. This makes sense – most of the economy that shut down due to COVID-19 and shelter-in-place orders are largely offline right now.

Over the next few weeks, we can expect that the parts of the economy that impact freight demand will start to come back online. Life won’t return to normal, but the trucking freight markets largely will. The reason is that the parts of the economy that are unlikely to return are the ones involved in sectors that generate little freight demand – concerts, events, sports. In other words, the really fun things that involve large gatherings. Travel is also expected to be all but shut down. All of this will come back eventually, but probably not until there is a coronavirus vaccine.

Restaurant dining will continue to suffer, but in regard to freight movement, demand is largely fungible between grocery and restaurants. In other words, people are still eating food, just from grocery or takeout versus dining at a restaurant.

Manufacturers and retailers will start to come back on board. This will be good for freight demand. There is a significant backlog of orders in manufacturing sectors that have been shut over the past few weeks. Even with demand being curtailed, this will return.

Two stressors are unemployment and consumer sentiment, but this is where the government has stepped up with unprecedented stimulus. The $2 trillion in fiscal stimulus coming from the White House and the estimated $4 trillion in stimulus coming from the Federal Reserve will cycle through our economy. And the U.S. isn’t the only country doing this. Countries all over the world are pumping massive amounts of money into the global economy.

And since consumers are not able to spend their money on experiences and fewer services, they will have more money to spend on goods. And there is one thing that consumers, especially Americans, will do is to spend their money.”

This is exactly what happened. Almost to a “T.”

At the time, many questioned my analysis and forecast of the market. Quite a few believed the U.S. economy would experience a multi-year downturn that would rival the Great Recession – or worse. Some of those same voices are calling me out now.

But I have confidence in our analysis. I wish the answers were different. I would prefer to say the U.S. trucking market was robust and the expansion will continue throughout 2022. But I can’t. Since I wrote the piece about the bloodbath, FreightWaves SONAR’s tender data continues to reinforce the perspective of a declining freight market.

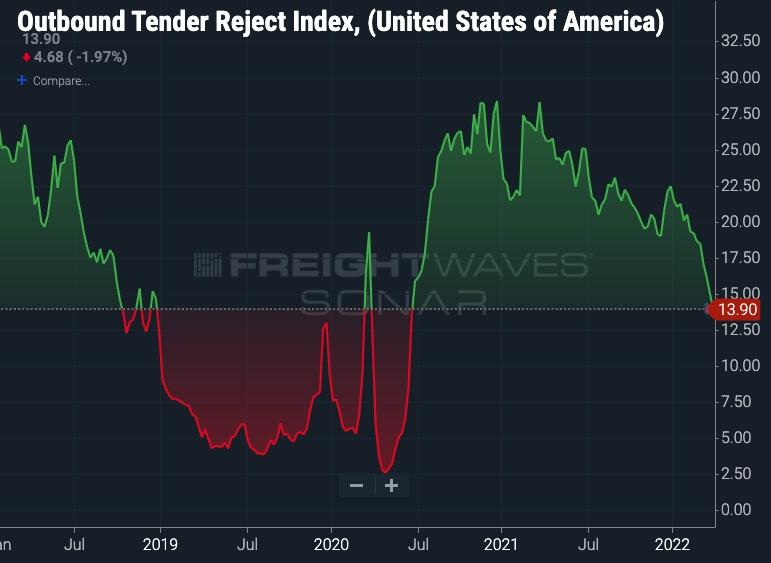

Tender rejections are the best indicator into real-time supply/demand in the truckload sector. The data comes from actual electronic load requests – “tenders” in the truckload contract market.

A high rejection rate means that trucking companies have more options to choose from. A low rejection rate means carriers have fewer options in freight to pick from. Since this measures actual load activity and not load board posts or searches, it tells us what the market is actually doing.

And since it measures the willingness of carriers that are contracted to accept or to reject a load they have a contracted rate for, if the rejection rate declines, it suggests capacity is loosening.

At the start of March, the rejection rate was 18.7% – today it sits at 13.90%. Even though it has only been a week since I wrote the “bloodbath” article, the rejection rate has fallen another 1.3%. The last week of March is normally one of the best weeks of the year for carriers, but this year it has been one of the worst.

Just wait for April…

{kind=link}

Tyler Durden

Fri, 04/01/2022 – 10:40