Hedges: The Slow-Motion Execution Of Julian Assange Continues Authored by Chris Hedges via Scheerpost.com, The decision by the High Court...

Read More

March Payrolls Miss: Fewest Jobs Added Since September, But Wages Come In Hot

In our NFP preview we said that only a catastrophic March jobs report coupled with even more negative data could shake the Fed’s determination to pursue a 50bps rate hike in May. Which is why despite a modest miss in the just reported March jobs data, we fail to see anything remotely ugly enough to change the big picture which sees the Fed continuing its liftoff as planned, with a 50bps hike next month.

Here’s what the BLS reported moments ago:

March Nonfarm Payrolls rose 431K and below the exp. 490K. This was also the lowest jobs increase since last September. However, the ~60K miss was more than offset by a 72K upward revision to February and a total 95K revision to the past two months:

The change in total nonfarm payroll employment for January was revised up by 23,000, from +481,000 to +504,000, and the change for February was revised up by 72,000, from +678,000 to +750,000. With these revisions, employment in January and February combined is 95,000 higher than previously reported.

Sectors that led payroll growth: leisure and hospitality, professional/business services, retail and manufacturing.

Overall, job growth averaged 562,000 per month in the first quarter of 2022, the same as the average monthly gain for 2021.

Employment is down by 1.6 million, or 1.0 percent, from its pre-pandemic level in February 2020

The establishment survey was strong; the Household survey was even stronger with the number of employed workers soaring by 736K in March to 158.458 million.

March Unemployment Rate Falls to 3.6% from 3.8%, below the exp. of 3.7%

Underemployment Rate 6.9%, down from 7.2%

Labor Participation Rate 62.4%, in line with exp. 62.4%, and above the 62.3% last

March Average Hourly Earnings Rise 0.4% M/M; Est. 0.4%, and up from an upward revised 0.1% in Feb;

March Average Hourly Earnings rose 5.6% vs Year Ago, higher than the est 5.5%

Average Weekly Hours All Employees 34.6, down from 34.7, and below the exp. 34.7

And visually:

{kind=link}

While there was some weakness at the headline jobs level, the market will gloss over this and instead focus on yet another month of red hot wage growth: average hourly earnings for all employees on private nonfarm payrolls rose by 13 cents to $31.73 in March. Over the past 12 months, average hourly earnings have increased by 5.6% In March, average hourly earnings of private sector production and nonsupervisory employees rose by 11 cents to $27.06. One reason for the stregnth, however, was purely statistical: the average workweek for all employees on private nonfarm payrolls fell by 0.1 hour to 34.6 hours in March.

{kind=link}

While that blistering increase in annual hourly earnings of 5.6% is basically the biggest jump in the current data series going back to 2007, it is still well below the 7.9% CPI rate meaning that inflation adjusted wages continue to decline.

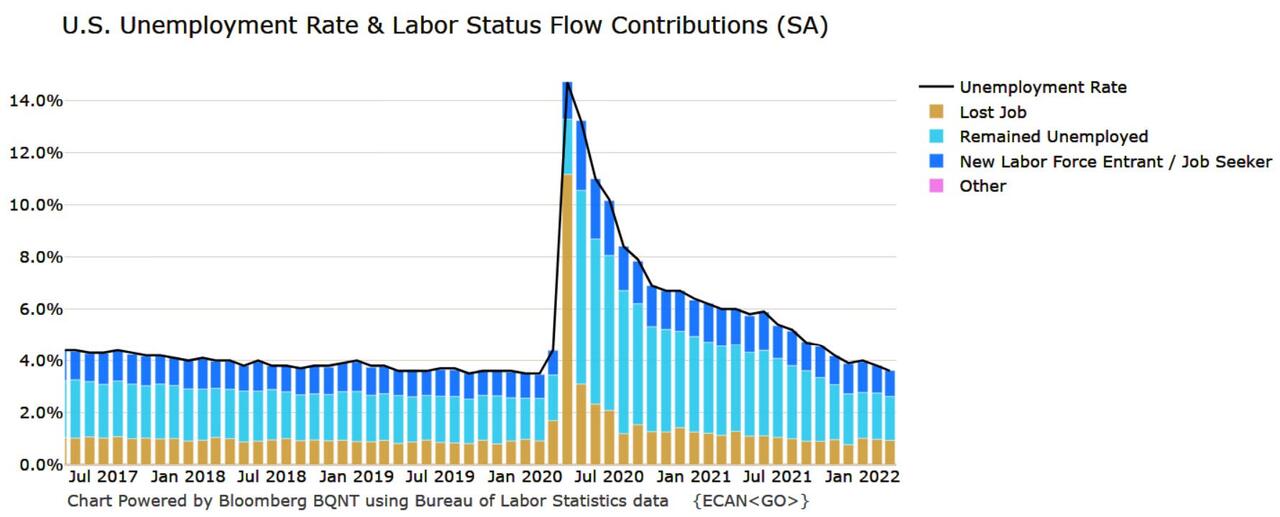

The unemployment rate declined by 0.2 percentage point to 3.6 percent in March, and the number of unemployed persons decreased by 318,000 to 6.0 million. These measures are little different from their values in February 2020 (3.5 percent and 5.7 million, respectively), prior to the coronavirus pandemic. The chart below shows the breakdown in the unemployment rate by labor status flows.

{kind=link}

Among the major worker groups, the unemployment rate for adult women (3.3 percent) declined in March. The jobless rates for adult men (3.4 percent), teenagers (10.0 percent), Whites (3.2 percent), Blacks (6.2 percent), Asians (2.8 percent), and Hispanics (4.2 percent) showed little change over the month, and unemployment fort his group is now below pre-covid levels.

{kind=link}

Some more details:

Among the unemployed, the number of permanent job losers decreased by 191,000 to 1.4 million in March and is little different from its February 2020 level of 1.3 million. The number of persons on temporary layoff was little changed over the month at 787,000 and has essentially returned to its February 2020 level. The number of job leavers fell by 176,000 to 787,000 in March.

In March, the number of long-term unemployed (those jobless for 27 weeks or more) decreased by 274,000 to 1.4 million. This measure is 307,000 higher than in February 2020. The long-term unemployed accounted for 23.9 percent of all unemployed persons in March.

The labor force participation rate, at 62.4 percent, changed little in March. The employment-population ratio increased by 0.2 percentage point to 60.1 percent. Both measures remain below their February 2020 values (63.4 percent and 61.2 percent, respectively).

The number of persons employed part time for economic reasons was about unchanged at 4.2 million in March and is little different from its February 2020 level. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

The number of persons not in the labor force who currently want a job increased by 382,000 to 5.7 million in March, following a decrease of a similar magnitude in the prior month. This measure is above its February 2020 level of 5.0 million. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

The underemployment rate for young adults aged 16 to 24 in March is 12.9%, according to Bloomberg calculations of Bureau of Labor Statistics data. Total unemployed aged 16-24 at 1,713,000. Marginally attached workers aged 16-24 at 264,000.

Meanwhile, the consequences of the covid pandemic are fading fast:

In March, 10.0 percent of employed persons teleworked because of the coronavirus pandemic, down from 13.0 percent in the prior month. These data refer to employed persons who teleworked or worked at home for pay at some point in the 4 weeks preceding the survey specifically because of the pandemic.

In March, 2.5 million persons reported that they had been unable to work because their employer closed or lost business due to the pandemic. This measure is down from 4.2 million in the previous month. Among those who reported in March that they were unable to work because of pandemic-related closures or lost business, 15.4 percent received at least some pay from their employer for the hours not worked, down from 20.3 percent in February.

Among those not in the labor force in March, 874,000 persons were prevented from looking for work due to the pandemic, down from 1.2 million in the prior month.

A breakdown of where the jobs were, via the Establishment Survey:

Employment in leisure and hospitality continued to increase, with a gain of 112,000 in March. Job growth occurred in food services and drinking places (+61,000) and accommodation (+25,000). Employment in leisure and hospitality is down by 1.5 million, or 8.7 percent, since February 2020.

Job growth continued in professional and business services, which added 102,000 jobs in March. Within the industry, job gains occurred in services to buildings and dwellings (+22,000), accounting and bookkeeping services (+18,000), management and technical consulting services (+15,000), computer systems design and related services (+12,000), and scientific research and development services (+5,000). Employment in professional and business services is 723,000 higher than in February 2020.

Employment in retail trade increased by 49,000 in March, with gains in general merchandise stores (+20,000) and food and beverage stores (+18,000). Health and personal care stores lost 5,000 jobs. Retail trade employment is 278,000 above its level in February 2020.

Manufacturing added 38,000 jobs in March. Employment in durable goods industries rose by 22,000, with gains in transportation equipment (+11,000) and electrical equipment and appliances (+4,000). These gains were partially offset by a loss of 5,000 jobs in nonmetallic mineral products. Nondurable goods manufacturing added 16,000 jobs over the month, including a gain in chemicals (+7,000). Since February 2020, manufacturing employment is down by 128,000, or 1.0 percent.

Employment in social assistance increased by 25,000 in March, with the gain concentrated in individual and family services (+18,000). Employment in social assistance is down by 126,000, or 2.9 percent, from its level in February 2020.

Employment in construction continued to trend up in March (+19,000) and has returned to its February 2020 level.

Employment in financial activities rose by 16,000, with gains in real estate and rental and leasing (+14,000) and in securities, commodity contracts, and investments (+5,000). Employment in financial activities is 41,000 above its level in February 2020.

Health care employment changed little in March (+8,000), after a large increase in the prior month. Employment in the industry is down by 298,000, or 1.8 percent, since February 2020.

Employment in transportation and warehousing was essentially unchanged in March (-1,000), following large gains in the prior 2 months. In March, a job gain in couriers and messengers (+7,000) was offset by small losses in other component industries. Employment in transportation and warehousing is 608,000 higher than in February 2020.

Commenting on the strong report, Bloomberg rates strategist Ira Jersey says the solid payroll report has caused the Treasury market to bear flatten:

“The report seems strong enough to extend fears that inflation will remain elevated, which could mean additional flattening until the CPI report later this month. Right now, the 2-year/10-year curve is priced to invert by 17 bps by this time next year – and we don’t see any reason to think that won’t happen well before the market is pricing.”

Bottom line, as we stated at the top and as Bloomberg echoes, “you have to think this cements a half-point Fed rate hike. Payrolls continue to advance, the jobless rate is nearing a decades-low level, and earnings are exploding. “

Tyler Durden

Fri, 04/01/2022 – 08:40

Recent Comments