42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Demand Destruction Has Begun

One month ago, Brent jumped above $100/bbl for the first time in eight years as Russia executed a full-scale invasion of Ukraine, and it became clear that western governments would impose sanctions. The oil market has been in triple digits for practically the entire time since.

And, after a month of oil prices we have not seen in nearly a decade and weeks of record-high fuel prices, JPMorgan has published a research report (available to pro subs) which finds that high-frequency data suggest that consumers are beginning to react resulting in what the Fed has desperately wanted to achieve all along: commodity demand destruction.

That said, high prices are clearly not the only demand-destructive force in the world at the moment, however. The crisis in Ukraine, crippling financial sanctions in Russia, and the continued spread of the highly infectious Omicron variant in China have an even more direct impact on regional fuel consumption than high prices.

As a result, JPMorgan has cut 1.1 mpd off its 2Q22 demand forecasts, followed by about 0.5 mbd cuts to both 3Q and 4Q. On net, this trims 420 kbd on average from the bank’s expectations for 2022 global oil demand as high prices, COVID restrictions, and geopolitical conflict drive demand destruction in Russia, China, India, and Europe.

While the US has been relatively isolated so far (despite the highest gasoline prices on record), JPM’s demand revisions are heavily concentrated in Europe, which remains the epicenter of the geopolitical shock. Since the start of the Russia-Ukraine war, the bank’s economists have downgraded the growth in the region by over 2%-pts and have raised inflation forecasts by nearly 3%-pts.

Moreover, after sliding sharply in February and bottoming in early March, COVID infections are up over 40% in the past two weeks across Europe with large increases across the UK, Germany, France, and Italy. Zero-tolerance COVID policy, combined with less effective vaccines and lack of natural immunity, presents a challenge to China’s growth outlook.

As a result, JPM now sees activity contracting in March and April, prompting a 1.1%-pts cut to China’s 2Q GDP growth. With the downward revisions to the Euro area and China, the largest US commercial bank now projects 1H22 global growth dipping below potential. Displaying limited sensitivity to near-term downside growth risks, major central banks continue to tilt hawkish. Chair Powell reiterated prospects for an accelerated pace of hikes and reinforced the notion that the Fed could soon start moving in 50bp increments. EM central banks also remain on the move.

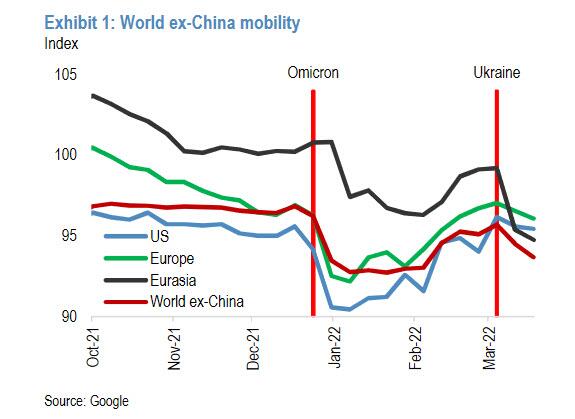

The clearest example of demand destruction can be seen in Eurasia, a region which includes both Russia and Ukraine, where mobility has fallen to its lowest level since early 2021.

{kind=link}

And in Europe, while mobility trends have reversed after a recovery from Omicron-driven lows earlier this year, they are now once again declining.

Consequently, JPM has cut its expectations for 2022 Eurasia oil demand by 270 kbd due to sanctions imposed on Russia. Eurasia demand for jet fuel will come in 130 kbd lower than the previous estimate as roughly half of Russian civil aircraft will end up grounded as a result of airspace bans and shortages of parts. JPM also revised Europe oil demand down by 160 kbd on average for 2022 due to sensitivity to high prices and lower expectations for economic growth in the region

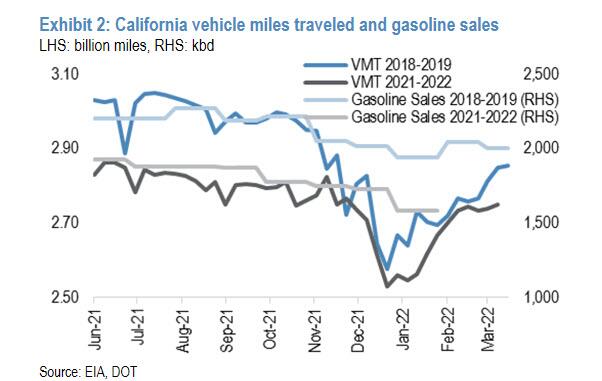

The good news is that for now, US mobility has been relatively resilient in spite of higher oil prices, but here too we are seeing the first signs of hampered driving demand recovery in California, where on-road fuel prices are more than $1.50 above the national average. California vehicle miles traveled (VMT) has been tracking closely to 2018-19 levels since late last year, but has deviated from the 2019 trend twice so far this year: once, as Omicron cases spread through the state, and again starting at the end of February.

{kind=link}

This flattening in VMT growth is likely due to the increase in gasoline prices following the Russian invasion and, while if this trend persists or spreads to other regions in the US, JPM said that it will likely revisit its assumptions for US fuel demand for 2022 as well.

JPM then does a similar exercise for China and India, and likewise cuts its forecasts for Q2 2022 oil demand there too (by 520kb/d and 120lb/s, respectively), and turns its attention to the mounting concerns over stability of Russian supplies.

Here, as reported previously, JPM finds that large quantities of Russian oil continue to be boycotted by Western refiners. Meanwhile, logistical issues are becoming entrenched as transport remains a significant challenge for Russian sales, with UK and European ports banning vessels flagged, operated or owned by Russia from docking at their ports. Reports of Saudi Arabia actively discussing pricing some of its oil sales to China in Yuan further point to difficulties facing Russia in shifting large volumes from Western consumers to China, where Saudi Arabia is a main supplier of crude. Given that Russia has very limited onshore storage capacity, a halt in exports would trigger production shut-ins within weeks, perhaps on an even larger scale than seen in April 2020.

Equally important are the developments in Kazakhstan— a country that ships around 1 mbd of its crude oil production through the CPC pipeline to the Russia’s Black Sea port of Novorossiysk. The pipeline was “damaged” on Tuesday, impacting around 1 mbd of export volumes for up to two months. The supply interruption was timed to coincide with the EU’s meeting on Thursday, prompting speculation that Moscow was prepared to retaliate against western sanctions by curbing both its own and Kazakh energy supplies, possibly leading to significantly larger disruptions than the current consensus base case assumes. Needless to say, finding alternative routes for all CPC volumes would be difficult, likely forcing the shut-in of fields in Kazakhstan. For now, JPM has removed 1 mbd from Kazakhstan’s April production.

Despite the nascent demand destruction, JPM writes that its baseline still assumes that the market’s current extreme aversion to Russian oil will subside. Volumetrically, this means that stranded Russian oil barrels will decline from 3.0-3.5 mbd in March to 2 mbd

in April and a perpetual 1 mbd thereafter, leading to Brent oil price averaging $114/bbl in 2Q22 and $101/bbl in 2H22, with prices rising over $120 in the interim.

That said, the bank’s commodity strategist recognize that the European consumer could force the governments’ hand as the human toll from Russia’s invasion mounts. Ominously, JPM cautions that as the single largest buyer of Russian oil, “the more rapidly Europe seeks to cut Russia’s imports, the higher global oil prices will rise” and in the event of a full 3.8 mbd drop in Russian exports, crude oil prices could soar to $185/bbl.

Of course, all of the above is predicated upon an “all else equal” framework, however as we have reported recently, it now appears that developed government such as the US, UK and Europe are planning to offset demand destruction with what gas stimmies or cutting gas taxes, what some have called “demand construction” which will achieve just the opposite of what it hopes to achieve as Bloomberg’s Kavier Blas noted two days ago: “Exactly the opposite that the current market requires. Rather than support poorer families, it goes for a blanket, regressive tax policy.“

OIL DEMAND ‘CONSTRUCTION’⛽️🚗🚛💶

Germany will cut tax on fuel for 3months by **30 cents of euro for gasoline** and **14 cents for diesel**, Finance Minister Christian Lindner said. Taxpayers will also receive a **one-off subsidy of €300** to help with energy costs | #OOTT

— Javier Blas (@JavierBlas) March 24, 2022

The UK government joins some European countries in “demand construction” for the oil market, lowering fuel taxes. Exactly the opposite that the current market requires. Rather than support poorer families, it goes for a blanket, regressive tax policy | #OOTT

— Javier Blas (@JavierBlas) March 23, 2022

Tyler Durden

Fri, 03/25/2022 – 20:00ZeroHedge News