Hedges: The Slow-Motion Execution Of Julian Assange Continues Authored by Chris Hedges via Scheerpost.com, The decision by the High Court...

Read More

Hedge Funds Sell Record 1 Billion Barrels In Oil Futures Just As Prices Explode Higher

By John Kemp, senior market analyst at Reuters

For the second week in a row, investors trimmed bullish petroleum positions amid elevated volatility, with prices oscillating between the twin threats posed by sanctions-driven supply disruptions and a demand-destroying recession.

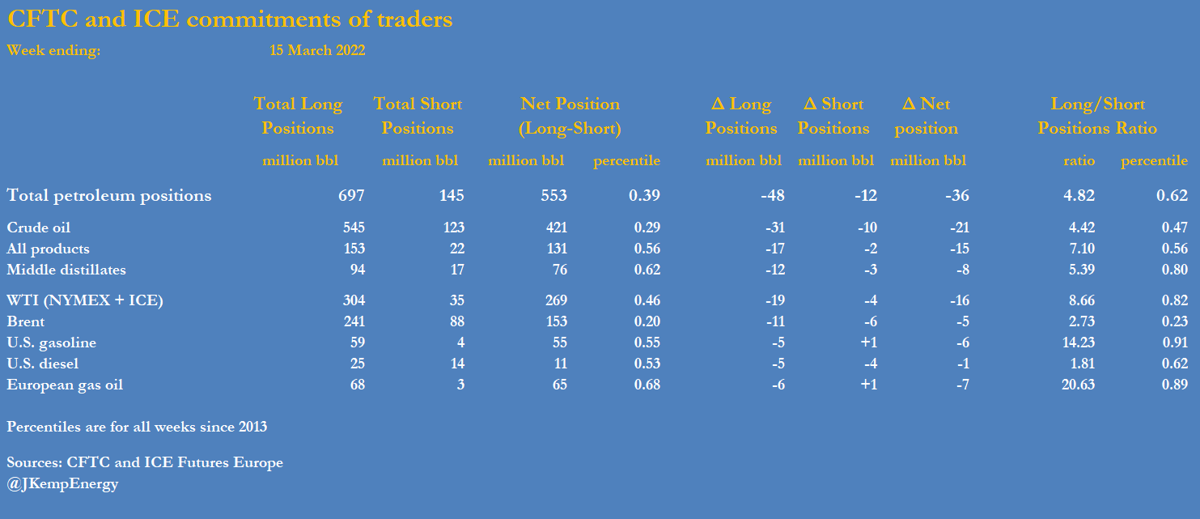

Hedge funds and other money managers sold the equivalent of 36 million barrels in the six most important petroleum-related futures and options contracts in the week to March 15.

{kind=link}

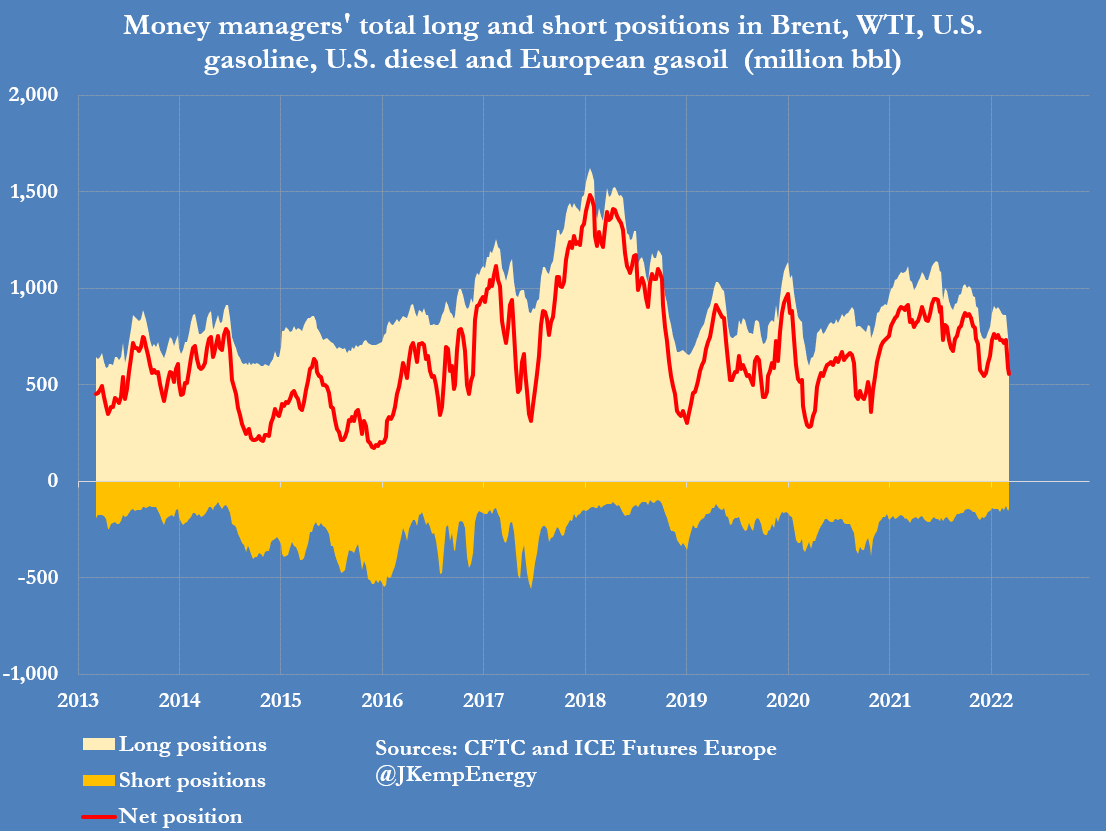

Fund sales have totalled 178 million barrels over the two most recent weeks, reducing their combined position to 553 million barrels, which is only in the 39th percentile for all weeks since 2013.

{kind=link}

Bullish long positions still outnumbered bearish short ones by 4.82:1 (62nd percentile) last week, but the ratio had been reduced sharply from 6.69:1 (84th percentile) two weeks earlier.

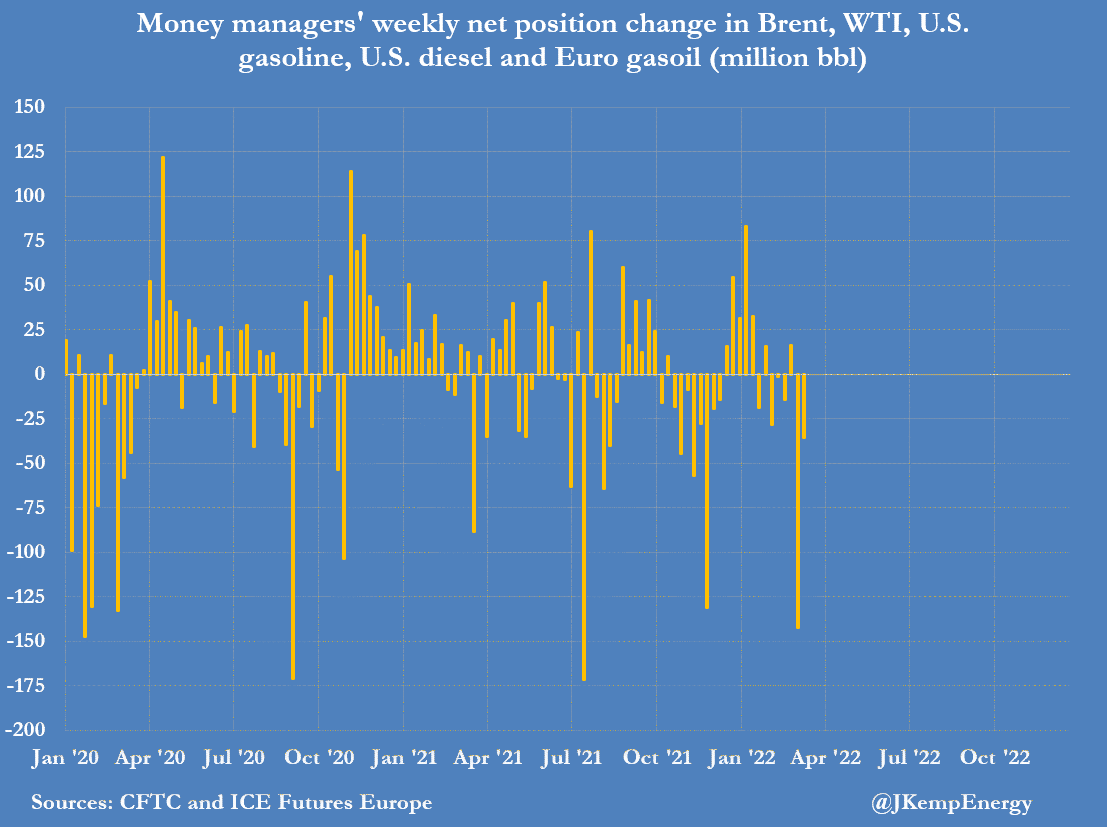

There was a reduction last week in both bullish long positions (-48 million barrels) and bearish short ones (-12 million) as fund managers reduced risk exposure in response to the heightened volatility.

{kind=link}

There were net sales across the board in NYMEX and ICE WTI (-16 million barrels), Brent (-5 million), U.S. gasoline (-6 million), U.S. diesel (-1 million) and European gas oil (-7 million).

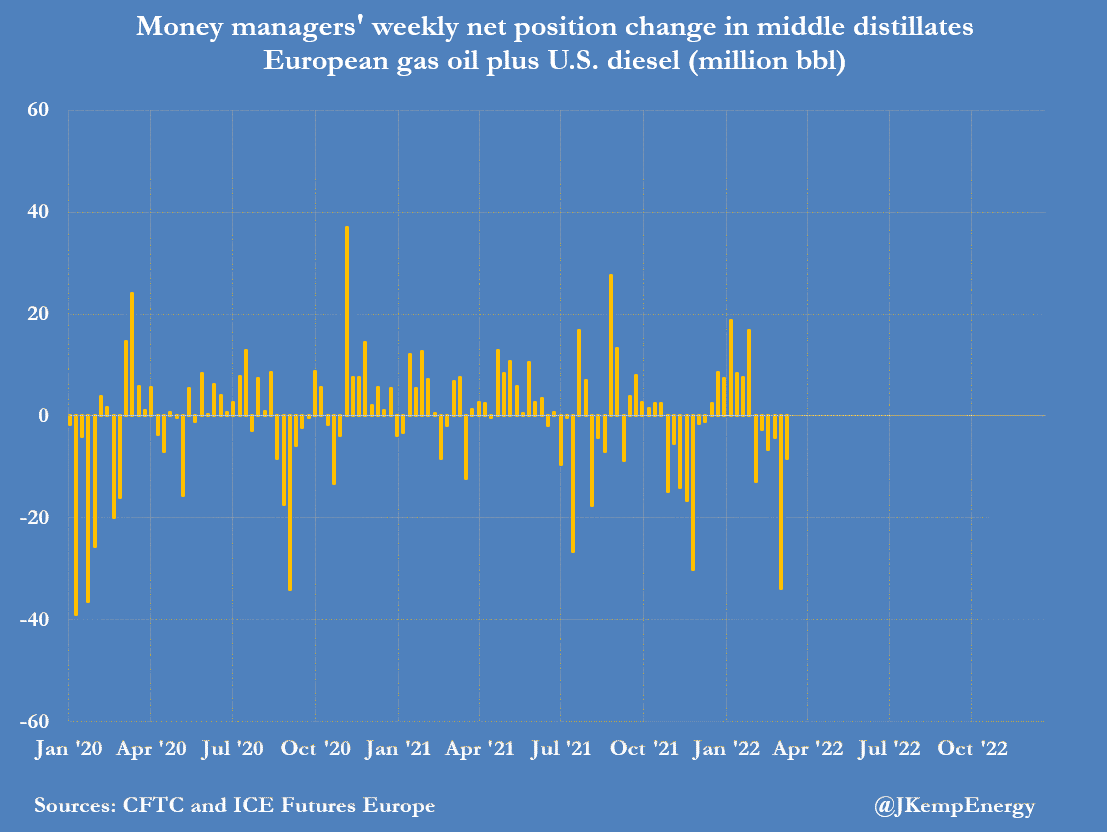

In response to the deteriorating economic outlook, portfolio managers have sold middle distillates for six consecutive weeks, reducing their bullish position by a total of 68 million barrels since Feb. 1.

{kind=link}

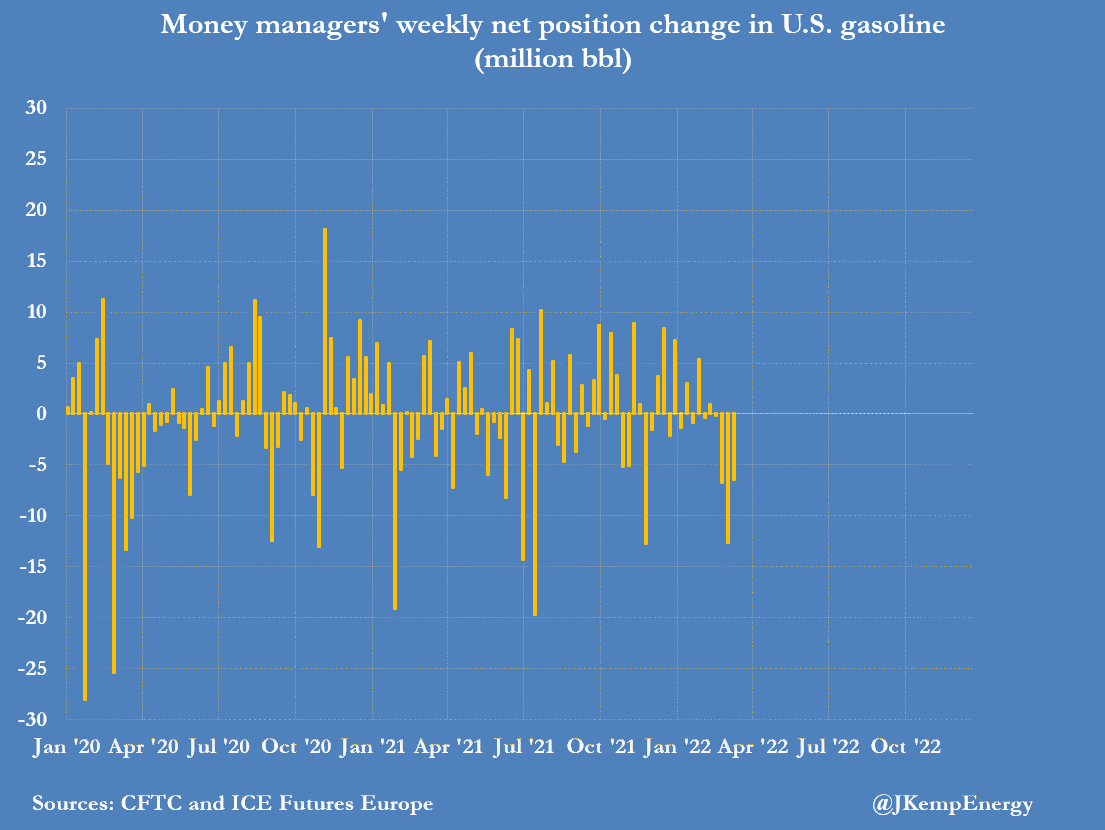

They have also sold gasoline for three weeks running, reducing their bullish position by a total of 26 million barrels since Feb. 22 in expectation that higher prices will keep more motorists off the roads.

{kind=link}

Russia’s invasion of Ukraine and the sanctions imposed in response by the United States and its European allies have threatened the largest loss of Russian oil exports and production from any country for decades.

But intensifying inflation, rising interest rates, pressure from higher fuel bills and continued coronavirus lockdowns in China have also raised risks of a recession and a big hit to oil consumption.

There is also extreme uncertainty about the course of the Russia-Ukraine conflict and the resulting sanctions on Russia’s crude oil, fuel oil and diesel exports.

The increased price volatility has triggered a massive rise in margin requirements, heightening the cost of maintaining existing futures and options positions or initiating new ones.

As a result, many market participants, not only hedge funds, have trimmed futures and options positions either out of caution or because they cannot fund the increased margin requirements.

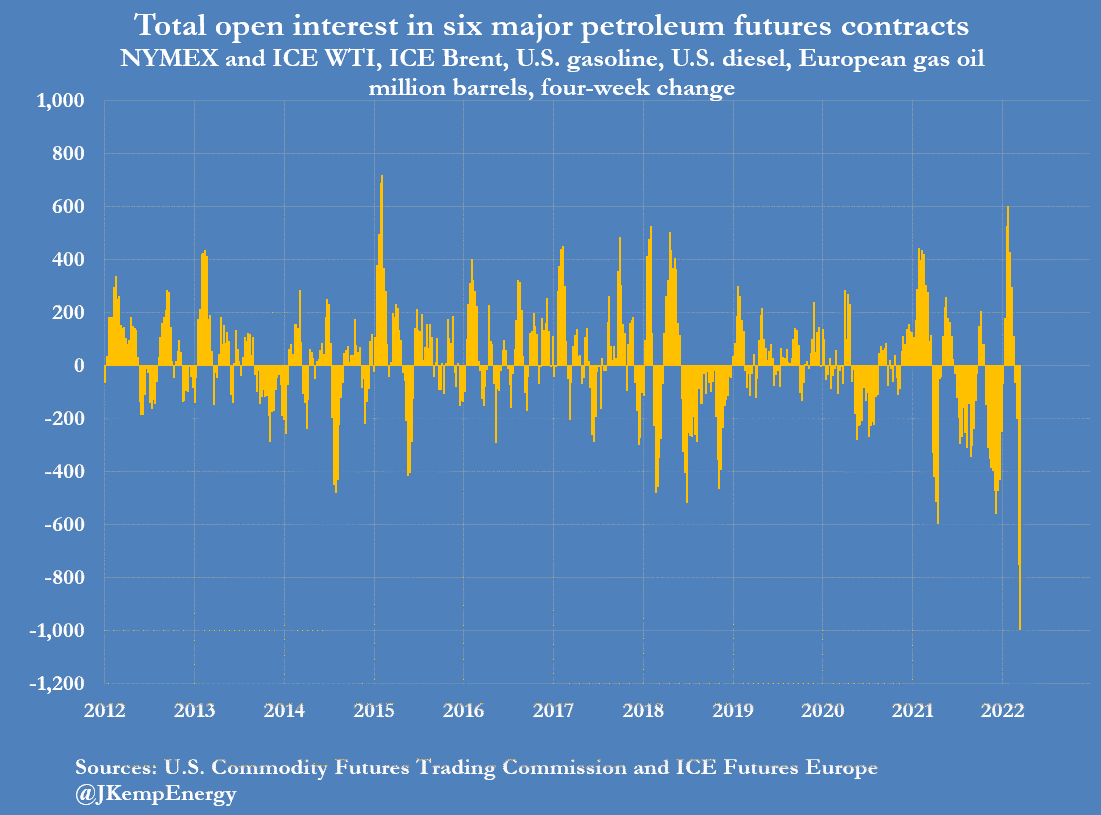

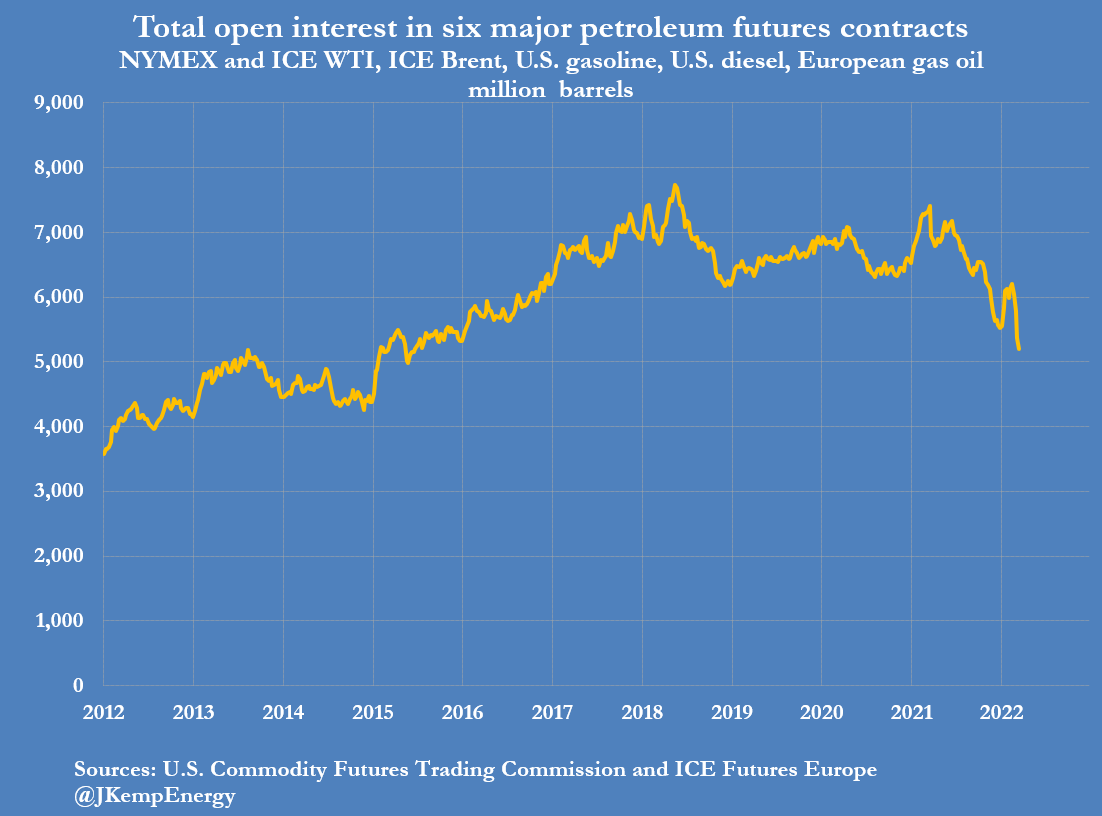

On the futures side, total open interest across the six major contracts has fallen by almost 1 billion barrels in the past four weeks…

{kind=link}

… a record rate of decline, to hit the lowest level since June 2015.

{kind=link}

Diminished market liquidity and heightened volatility have fed off one another in a classic positive feedback loop, leading to large price swings as traders struggle to assess competing upside and downside price risks.

Tyler Durden

Mon, 03/21/2022 – 15:12

Recent Comments