Hedges: The Slow-Motion Execution Of Julian Assange Continues Authored by Chris Hedges via Scheerpost.com, The decision by the High Court...

Read More

Just As All Hope Seemed Lost, China Reports Miraculously Good Economic Data

Going into Tuesday, all hope seemed lost in China.

First, China reported a whopping 5,154 new covid cases (3,507 new local confirmed Covid cases and 1,647 asymptomatic cases) for Monday, well more than double from the day before, and confirming that the country’s covid troubles – which over the past 48 hours led to the lockdown of Shenzhen and other cities – are only getting worse. So worse, in fact, that questions have emerged: how did China not report more than 100 cases on any one day for two years, and then now – with the Ukraine war raging – Beijing is suddenly locking down key US supply chain arteries.

For the past two years, China had at most 50-100 new daily covid cases. Now it’s 5000, and it is shutting down key supply chain arteries that feed the US economy.

So bizarre

— zerohedge (@zerohedge) March 15, 2022

Second, for the second day in a row, the PBOC fixed the yuan more than 100 pips weaker than expected, as the central bank telegraphs it will no longer tolerate a weak currency, relentless capital inflows be damned, as the country remembers that it is after all, an export-driven mercantilist which above all, needs a favorable exchange rate.

{kind=link}

Third, one day after Chinese stocks traded in HK suffered their biggest drop since 2008, we are bracing for another major crash:

ALIBABA SHARES INDICATED 9.8% LOWER IN HONG KONG

MEITUAN SHARES INDICATED 11% LOWER IN HONG KONG

Elsewhere, China’s CSI 300 Index tuimbled 2.5%, while the Shanghai Composite declined 2.4% and the Hang Seng fell 3.7%, while the Hang Seng Tech Index lost as much as 7.2% soon after open Tuesday, and is now down almost 40% in under a month.

{kind=link}

Why? Because contrary to expectations set by the PBOC itself (via its own media mouthpiece), the PBOC decided to keep the MLF rate unchanged despite an intensifying rout in nation’s equities, adding to investor concerns from lockdowns to geopolitical and regulatory risks.

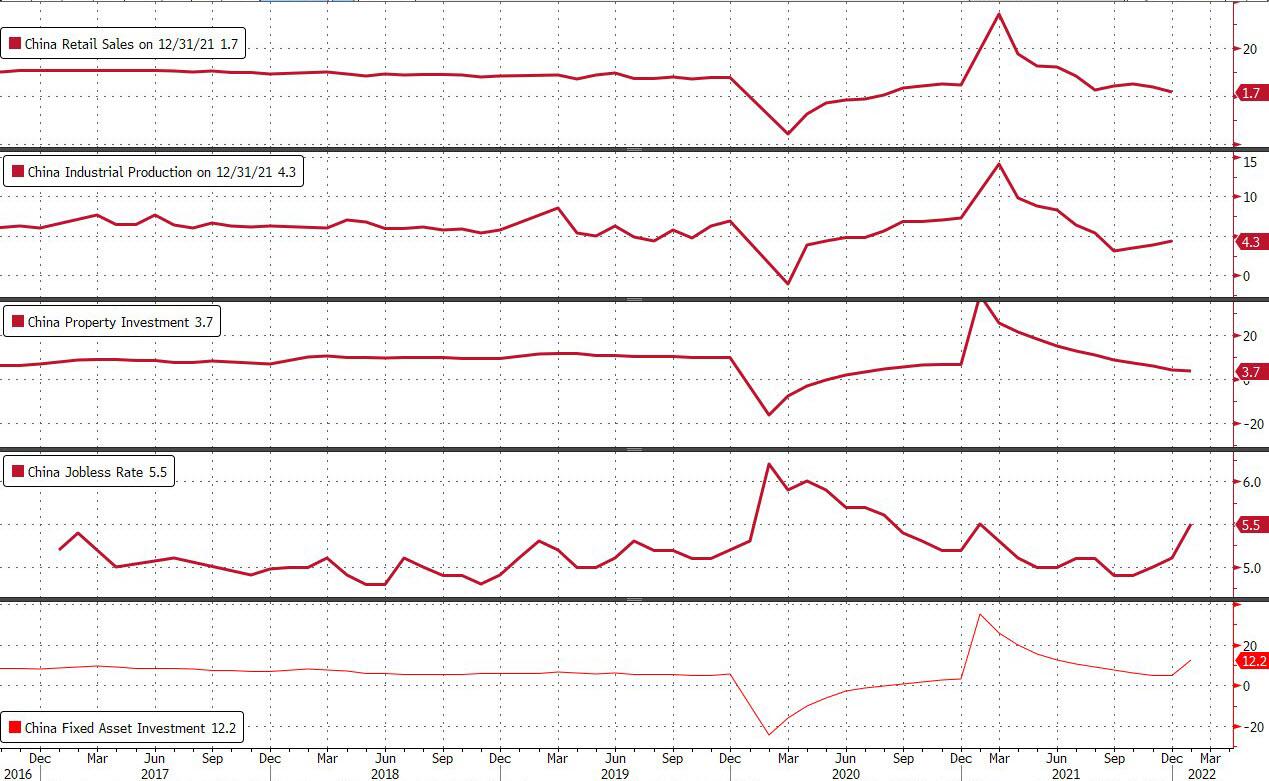

And then, as even the firmest China believers were getting ready to throw in the towel, moments ago the National Bureau of Statistics reported a trio February economic numbers that were so ridiculously good they were, well… simply ridiculous. To wit:

Jan.-Feb. Industrial Output +7.5%, y/y, smashing estimates of +4%, printing above the highest economist forecast (range +3.2% to +5.5%, 24 economists) and far higher than the Ded +4.3%.

Jan.-Feb. Retail Sales +6.7% y/y; smashing est. +3%, printing above the highest economist forecast (range +1.5% to +5.5%, 23 economists), and far, far higher than the Dec. +1.7%

Jan.-Feb. Fixed-Asset Investment excluding rural households +12.2% y/y; smashing est. +5% and also printing above the highest economist forecast (range +3% to +9%, 29 economists) as well as more than 2x higher than Jan.-Dec. +4.9%

{kind=link}

While the above data was the most closely watched, not all the data was flawless:

Jan.-Feb. property investment +3.7% y/y vs +4.4% in Jan.-Dec.

Jan.-Feb. residential property sales -22.1% y/y vs +5.3% in Jan.-Dec.

End- Feb. surveyed jobless rate 5.5% vs 5.1% end-Dec.

Then there were the tertiary data:

China Jan.-Feb. Power Output Rose 4% Y/y to 1314.1b kwh

China Feb. Power consumption rises 16.9% Y/Y, to 623.5 billion kilowatt-hours (kWh), the state TV reports, citing the National Energy Administration.

Power output in Jan.-Feb. rose 4% y/y to 1314.1b kwh

Crude processing in Jan.-Feb. fell 1.1% y/y to 113.01m tons

Crude oil output in Jan.-Feb. rose 4.6% y/y to 33.47m tons

Natural gas output in Jan.-Feb. rose 6.7% y/y to 37.2bcm

Ethylene output in Jan.-Feb. rose 3.9% y/y to 4.87m tons

Coal output in Jan.-Feb. rose 10.3% y/y to 686.6m tons

China’s apparent oil demand, which includes oil processing volume and net imports of refined oil products, remained stable in the first two months of the year, despite higher prices: China’s apparent oil demand rose 2.89% in January-February from a year earlier, to 13.710m b/d.

A closer read of the data hints that not all was as strong as indicated: the growth in retail sales was driven by a surge in petroleum and jewelry which saw the highest increase across all categories. That, as Bloomberg notes, could be the impact of price increase, instead of volume.

Still, the fact that the big 3 were so stellar should placate those who are seeing a collapse (even if nobody actually believes these numbers).

So why did Beijing report such ridiculous prints? Well, one possible reason is to justify the PBOC’s decision earlier in the session to hold the key, MLF interest rate unchanged instead of cutting it as analysts expected.

Either that, or to justify what would be a powerful Plunge Protection intervention immediately after the data, and sure enough:

*HANG SENG TECH INDEX ERASES LOSS OF AS MUCH AS 7.2%

*TENCENT PARES LOSS TO 0.5% FROM AS MUCH AS 8%

And as goes China, so go US equity futures…

{kind=link}

Tyler Durden

Mon, 03/14/2022 – 22:40

Recent Comments